Your Plan Survived 1,000 Futures. Did It Survive the Worst 50?

Average success hides the tail. We stress-test against the ugliest outcomes, not just the median.

The first time our plan came back with a 95 percent success rate, we high-fived. Then Mayur, who cannot leave a good number alone, asked the uncomfortable follow-up: what happens in the other 5 percent? With a thousand simulated futures, 5 percent is fifty futures where the plan fails. Fifty versions of us run out of money. The headline number had felt like a finish line, but it was actually pointing at a door we had not opened. The real question for a retiree is not "how often do I succeed," it is "what does failure look like, and could I live through it."

Why one big number is not enough

A success percentage is a genuinely useful summary. It runs your plan across a thousand possible market futures and tells you the share in which you do not run out. We rely on it. But a single percentage flattens an enormous amount of information, and the part it flattens is exactly the part that should keep you honest: the tail.

Two plans can both show 90 percent success and be nothing alike. In one, the 10 percent of bad cases miss by a hair, running low only in the final years. In the other, the bad cases collapse a decade early and leave you destitute in your seventies. Same headline. Wildly different risk. The average success rate cannot tell them apart. Only looking at the worst outcomes can.

Read the bottom of the distribution

This is why we spend more time on the bad cases than the good ones.

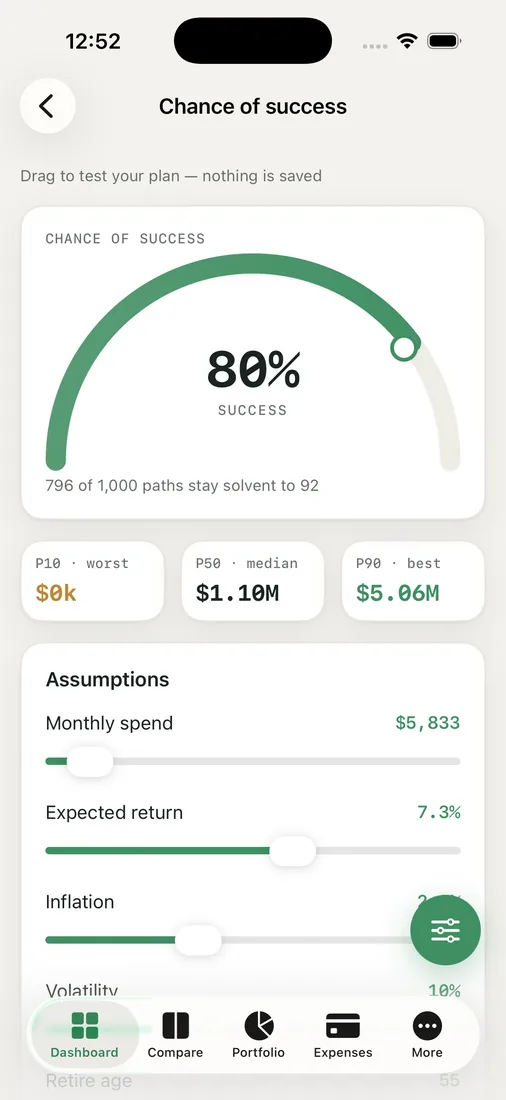

The chance view in RetireOdds gives us the success gauge, but it also shows the P10, P50, and P90 bands, all in today's dollars. P50 is the median, the typical path. P10 is the unlucky tenth, the bottom of the realistic range. We treat P10 as the number that actually matters, because a plan we can only afford if we land at or above the median is not a plan we can afford. The honest test is whether we can survive the bottom of the distribution, not the middle.

And we do not lean on a single engine to draw that bottom. There are three: a random-normal Monte Carlo, a bootstrap of real US market history, and a historical-sequence backtest that replays actual past sequences in order. When all three agree the tail is survivable, we relax. When the historical backtest carves a deeper hole than the smooth simulation, we listen, because real history clustered its bad years in ways a tidy bell curve never will.

What we actually do with the bad fifty

Opening that door turned out to be empowering rather than scary, because the bad cases are where you find the levers.

- If the worst paths fail early, a cash buffer that prevents forced selling in the first downturn often lifts the whole tail.

- If they fail from spending pressure, building in some flexibility, trimming outflows in bad years, can move failures back into successes.

- If they fail from an early crash, adjusting the allocation around our retirement date can shrink the damage.

Each of those we can test the same way, by re-running and watching whether the tail, not just the average, improves.

For our cross-border, multi-currency life, the tail is especially worth respecting, because a bad market and a bad exchange-rate swing can arrive together and stack. A plan that only works in calm waters was never going to survive the way we actually live, which is a large part of why we built RetireOdds to show the ugly outcomes plainly instead of burying them under one cheerful percentage.

We are not forecasting disaster, and a high success rate is a good thing. The point is that the worth of a plan is decided at its weakest point, not its average. Look at the bottom fifty before you trust the top nine hundred and fifty.

Key takeaways

- A success percentage is useful but flattens the tail, and the tail is where a retirement plan actually lives or dies.

- Two plans with the same success rate can have very different failure modes, so read the P10 band, not just the median.

- Running multiple engines, especially a historical-sequence backtest, reveals tail weakness a smooth simulation can hide.

- The bad cases are where the levers are: a cash buffer, spending flexibility, and allocation can all lift the worst outcomes.

Before you trust your headline number, open the door on the bad cases. Run your own odds and check whether your plan survives the worst, not just the average.