Same Plan, Opposite Outcomes: Sequence Risk

Retiring into 1966 vs. 1982 produced wildly different results on identical assumptions. Why timing rules.

Here is a comparison that rearranged how we think about retiring. Take two people with identical savings, identical spending, identical allocation, and the same long-run average market return. The only difference is the calendar. One retires in 1966. The other retires in 1982. Run the history forward and one of them comes close to running out of money, while the other dies rich. Same plan. Opposite outcomes. The variable was not skill or savings. It was timing.

The 1966 problem

The retiree who stopped working in 1966 walked straight into a grim stretch. The late 1960s and 1970s brought a punishing combination: weak real stock returns and high inflation that ate away at spending power year after year. Withdrawing a steady income from a portfolio that was flat or falling, while prices climbed, is corrosive. Every withdrawal in a down year sells shares that never come back, and inflation quietly forces the dollar amount of those withdrawals higher.

By the time the market finally recovered, the 1966 retiree had already sold off a chunk of the portfolio at bad prices. The recovery came too late to fully repair the damage.

The 1982 gift

The 1982 retiree got the mirror image. They retired right as one of the great bull markets in history was getting started. Their early withdrawals came out of a portfolio that was climbing, so the money they spent was more than replaced by growth. By the time any rough patches arrived, the portfolio had a huge cushion. Same withdrawal rate, same assumptions, completely different ending, because the good years came first instead of last.

This is sequence-of-returns risk in its purest historical form. It is not a textbook abstraction. It is two real decades that produced opposite fates for the same plan.

Why averages lie to retirees

A plan built on an average return implicitly assumes the good and bad years are evenly distributed and harmless in their ordering. For a saver, that is roughly fine. For a retiree pulling money out, it is dangerously incomplete, because withdrawals turn an early downturn into permanent lost shares. The same volatility that is noise to a saver is destiny to a retiree.

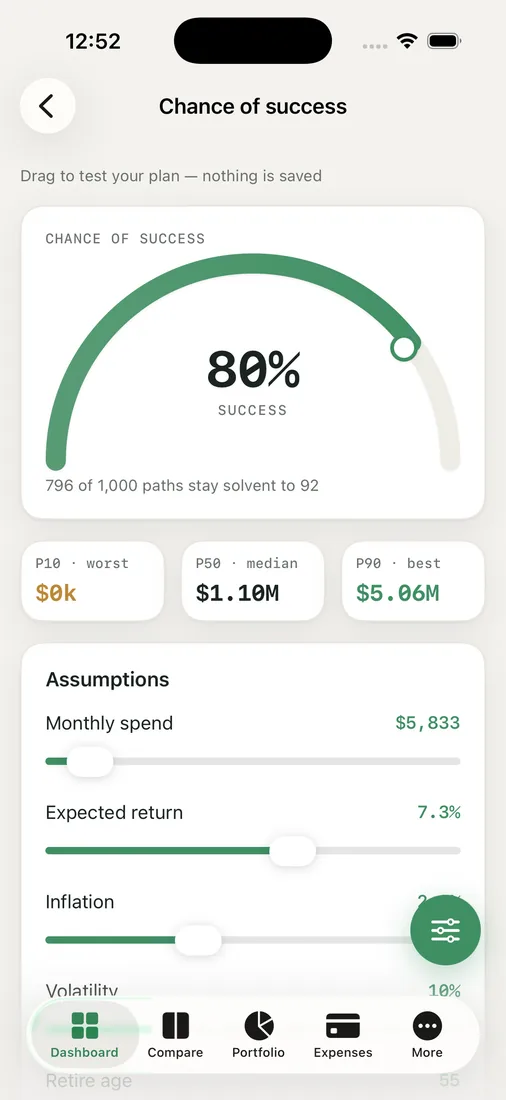

That is exactly why we never trust a single projection line for our own plan.

The chance view in RetireOdds tackles this head-on with three different engines. There is a random-normal Monte Carlo, a bootstrap that resamples real US market history, and, most relevant here, a historical-sequence backtest that replays actual past sequences in their real order, 1966 included. That last engine is the one that would have shown the 1966 retiree their trouble in advance, because it preserves the actual clustering of bad years instead of averaging it into a smooth, falsely reassuring line.

We run all three and compare. When they roughly agree, we feel steadier. When the historical backtest is noticeably harsher than the smooth simulation, that gap is the warning. It is telling us our plan leans on the bad years being polite.

For our family, the lesson is not to fear retiring, it is to refuse to assume we will be the 1982 retiree. We cannot pick our calendar. We can only build a plan that would have survived 1966 too, with enough flexibility, buffer, and margin that an ugly first decade bends us without breaking us. That mindset, plan for the bad sequence and be pleasantly surprised by a good one, is the whole reason we look at distributions instead of a single hopeful average.

We are not predicting the next 1966 or 1982. Nobody can. The point is that your retirement date is partly a roll of the dice you do not control, so the smart move is to test your plan against the sequences that broke people before.

Key takeaways

- Two retirees with identical plans can end up worlds apart purely because of when the bad market years arrived, as 1966 vs. 1982 shows.

- Withdrawals turn an early downturn into permanently lost shares, which is why ordering matters far more in retirement than in saving.

- A single average-return projection hides this entirely; you need to see the range of sequences.

- A historical-sequence backtest preserves real bad-year clustering, so it can reveal weakness a smooth simulation papers over.

You cannot choose your retirement-year sequence, but you can stress-test against the worst ones. Run your own odds and see whether your plan would have survived a 1966.