Roth Optimizer v2: Conversion Schedules Priced Honestly

The Roth Optimizer now prices IRMAA's two-year lag and ACA subsidy loss into every conversion schedule it proposes, not just the bracket.

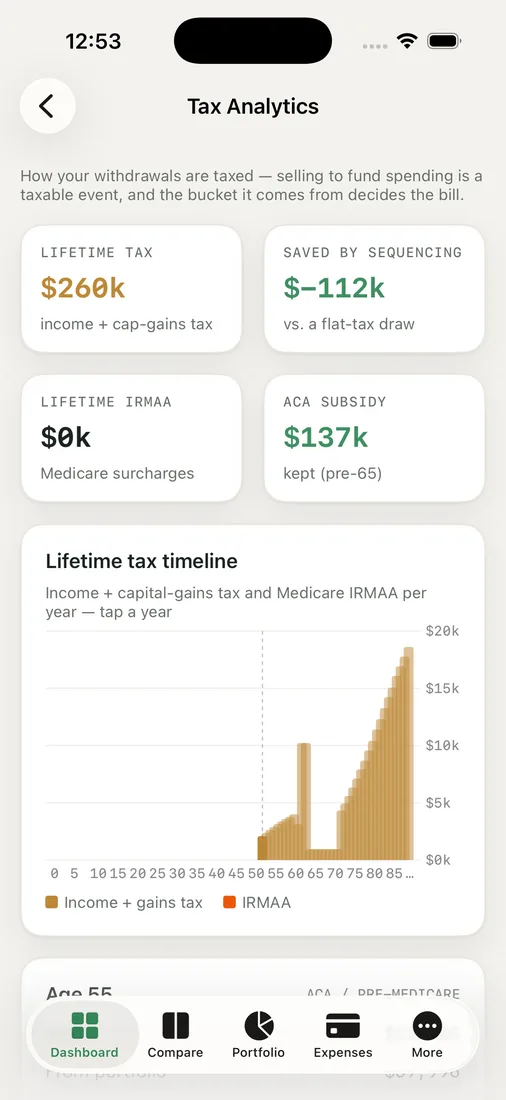

A forum post convinced me, a couple of years back, to convert "up to the top of the 22 percent bracket" every year until Medicare kicked in. Clean rule, easy to follow, and it ignored two things that showed up on our doorstep anyway: a Medicare premium surcharge that arrived two years after the conversion that caused it, by which point I had forgotten the conversion was the reason, and a health insurance subsidy that quietly shrank the same year we converted, because the rule only ever looked at the bracket. Mayur pulled both statements out and asked why a "top of the bracket" rule doesn't know either exists. It doesn't, because it isn't actually modeling your year, it's modeling a number line. That's what the Roth Optimizer's second version fixes.

Searching schedules, not years

The Roth & Tax Optimizer doesn't ask you to pick one conversion amount for one year. It searches over multi-year conversion schedules aimed at an explicit objective you set, and it tests each candidate schedule against your actual plan, not a generic case pulled from a forum thread.

The frictions most rules of thumb skip

The v2 point is that "top of the bracket" was never the full cost of a conversion, and the optimizer now prices the parts that rule leaves out:

- IRMAA's two-year lag. The Medicare surcharge that a conversion triggers doesn't land the year you convert — it lands two tax years later, on the statutory lookback. A schedule that looks clean this year can be expensive two Aprils from now, and the optimizer accounts for the delay instead of pretending the bill is due immediately or never.

- ACA subsidy erosion. If you're on an ACA plan before Medicare, a conversion can shrink or wipe out the subsidy in the years you convert, and that cost gets weighed alongside the tax itself.

- How far each bracket actually fills. Not just whether you're "in" the 22 percent bracket, but how much room is genuinely left in it this year, given everything else already stacked into your income.

Constraints that get named, not hidden

Two practical checks run alongside every schedule, and both are things a rule of thumb has no way to know. First, whether there's actually cash on hand to pay the conversion tax without pulling money back out of the Roth you just funded, which would defeat the purpose. Second, a breakeven age — if you're unlikely to live long enough for a given conversion to pay off, the optimizer says so rather than quietly recommending it anyway.

When a schedule fails one of those constraints, it doesn't just disappear from the results. The failure is named, so you can see why a schedule that looks attractive on paper got ruled out, instead of wondering where it went.

One ledger, not a guess

Underneath all of it, the conversion tax for every candidate schedule is computed on the same shared annual tax ledger that runs the rest of your plan, stacked with whatever other income that year already has — Social Security, pensions, RMDs, everything. It is never estimated as a flat rate applied to the conversion amount alone, which is the shortcut that let our old forum rule miss IRMAA and ACA in the first place. This is modeling, not tax advice, and the honest answer for a specific schedule still depends on numbers only your own return will settle.

Key takeaways

- The Roth Optimizer searches multi-year conversion schedules against an objective, tested on your actual plan.

- It now prices IRMAA's two-year lag and ACA subsidy erosion, not just which bracket a conversion lands in.

- Cash-to-pay and breakeven-age constraints are checked, and a failing schedule is named as failing, not silently dropped.

- Every conversion's tax runs through the shared annual ledger, stacked with your real other income, never a flat guess.

Run the optimizer against your own numbers before you copy anyone's bracket rule.