529 vs. Retiring on Time

Every dollar into a 529 is a dollar not funding your own retirement. How we balance the two goals.

A few months ago we sat down to top up the college savings for our older one, who turns 15 next year. The advisor's spreadsheet suggested we should be putting away about $1,800 a month per child to fully fund four years at a private US university. We did the multiplication for two kids over the next decade and felt our stomachs drop. That money has to come from somewhere, and the only place it could come from was the same pile we've been building for five years to retire early.

That's the quiet tension nobody warns you about. There is no separate "college account fairy." Every dollar you route into a 529 is a dollar that isn't compounding toward your own freedom date.

The trade-off in plain English

A 529 plan is a tax-advantaged account for education: contributions grow tax-free and come out tax-free when spent on qualified costs. It's a genuinely good deal. But it competes directly with your retirement savings for the same monthly surplus, and the two goals pull in opposite directions.

Fund college aggressively and your own retirement date slides to the right. Fund retirement first and you may face the bill with loans, scholarships, or a kid who works part-time. There's an old piece of wisdom here that we keep coming back to: you can borrow for college, but nobody will lend you money to retire.

For us as expats it's messier still. We've moved US to Thailand to Singapore to Spain, and our kids may not attend a US school at all. European public universities can cost a fraction of the American sticker price. So the "right" number to save isn't one number — it's a range, and the range is enormous.

How we actually weigh it

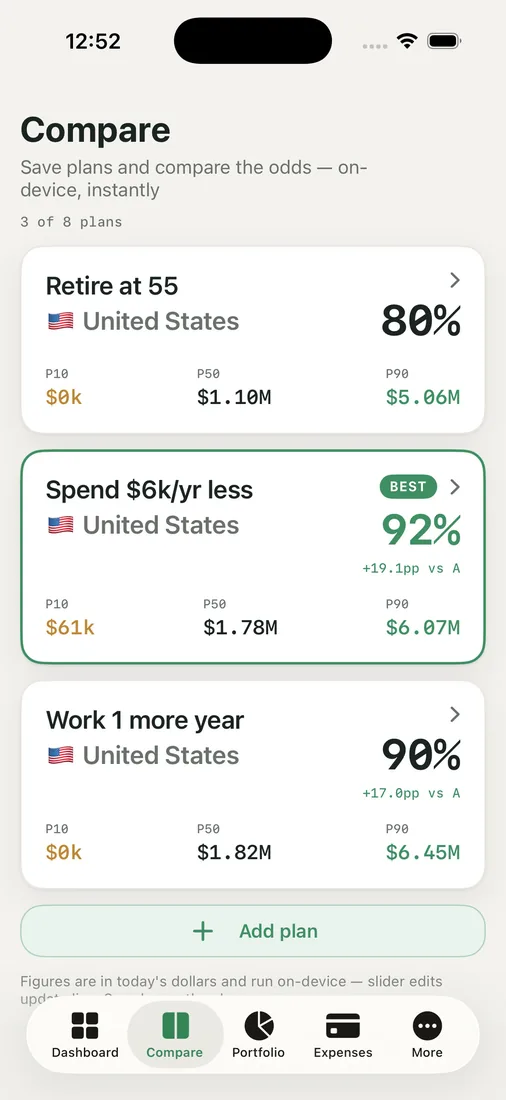

Rather than argue about it over dinner, we modeled it. We built two versions of our plan in Compare Plans and put them side by side.

- Plan A — College first. We front-load the 529s at roughly $1,800 a month per child and let our retirement contributions drop to make room.

- Plan B — Retire on time. We cap college savings at a level we're comfortable with — enough to cover a public-university path — and protect the retirement contribution.

Each plan came back with its own success percentage and a "BEST" badge on the stronger one. The gap was smaller than we feared. Front-loading both 529s pushed our modeled retirement date out by a little over two years and shaved several points off our long-run odds. Capping college savings barely dented the odds while still funding a realistic, non-catastrophic path for the kids.

Seeing both outcomes on one screen turned a values argument into a numbers conversation. We weren't choosing between loving our kids and loving our freedom. We were choosing between two specific, survivable plans — and we could see exactly what each one cost.

The middle path we landed on

We didn't pick either extreme. We funded the 529s to a "floor" that covers a public or in-state-equivalent education, then directed the rest to retirement. The logic: a partially funded 529 plus our kids having some skin in the game (summer work, merit aid, maybe a cheaper first two years) is a far better outcome than two fully funded 529s and parents who can't stop working until 60.

We also keep one principle front of mind. Retirement underfunding is silent and permanent; college underfunding is loud and solvable. If we're short on tuition, we'll know exactly when and we'll have options. If we're short on retirement at 65, the options have mostly expired.

We re-run the comparison every year as the kids get closer and our picture sharpens. What looked terrifying on the advisor's spreadsheet became manageable the moment we could see both futures next to each other.

Key takeaways

- A 529 and your retirement draw from the same monthly surplus — funding one delays the other, so model them together, not separately.

- Put the two versions of your plan side by side and compare the success percentage; the cost of "college first" is usually a concrete number of years, not a vague feeling.

- You can borrow for college; you can't borrow to retire. Protect the goal with no backup plan first.

- A funded floor plus scholarships, work, and cheaper school options often beats fully funding college at the expense of your own freedom date.

Curious what helping the kids actually costs your timeline? Run your own odds and see both futures side by side.