The $300k Tuition Bill vs. Your Nest Egg

Two kids through college is a second mortgage. We put the bill on the same timeline as retirement.

We did the math on a napkin in a café in Valencia and then sat there a little stunned. Two kids, four years each, at the kind of US universities they're aiming for — call it $75,000 a year all-in, times eight kid-years. Even with grants and the parts they'll cover themselves, the number we have to plan around is somewhere near $300,000. That's not a line item. That's a second mortgage, taken out twice, payable right when we plan to stop earning. The napkin made it real in a way two separate spreadsheets never had.

A second mortgage you can't refinance

It helps to call the $300,000 what it is. It's a debt-sized obligation — comparable to a whole house — except it doesn't come with a thirty-year amortization. It arrives in a tight cluster of years, mostly concentrated when our kids are 18 to 25, which for us lands squarely on top of early retirement.

And unlike a mortgage, there's no neat monthly payment that spreads the pain. College bills hit in big annual lumps. If we're already drawing down a portfolio to live on, those lumps come straight out of the same account, in the same years, often regardless of what the market is doing. A $75,000 withdrawal in a down year, on top of normal living expenses, is exactly the kind of shock that can leave a permanent dent.

That's the real danger of treating tuition as a someday problem. It isn't a vague future cost — it's a concrete, near-term, very large one that collides with the most fragile phase of the whole plan.

Put the bill on the timeline

So we stopped treating the nest egg and the tuition bill as two stories. We put them on one.

In the plan, we model each year of college as what it is: a large, dated expense landing in a specific year, in today's dollars so it inflates forward honestly. Suddenly the abstract $300,000 becomes a visible spike — actually two overlapping spikes — sitting right on the timeline next to our retirement spending and our portfolio balance.

Seeing it drawn out changed the conversation entirely. We could watch the nest egg dip through the tuition years and then — in the healthy scenarios — recover afterward, because the spike, while brutal, is temporary. The portfolio takes the hit and keeps going. In the weaker scenarios, we could see it not recover, and understand precisely which years and which market conditions caused the trouble. That's far more useful than a single yes-or-no verdict.

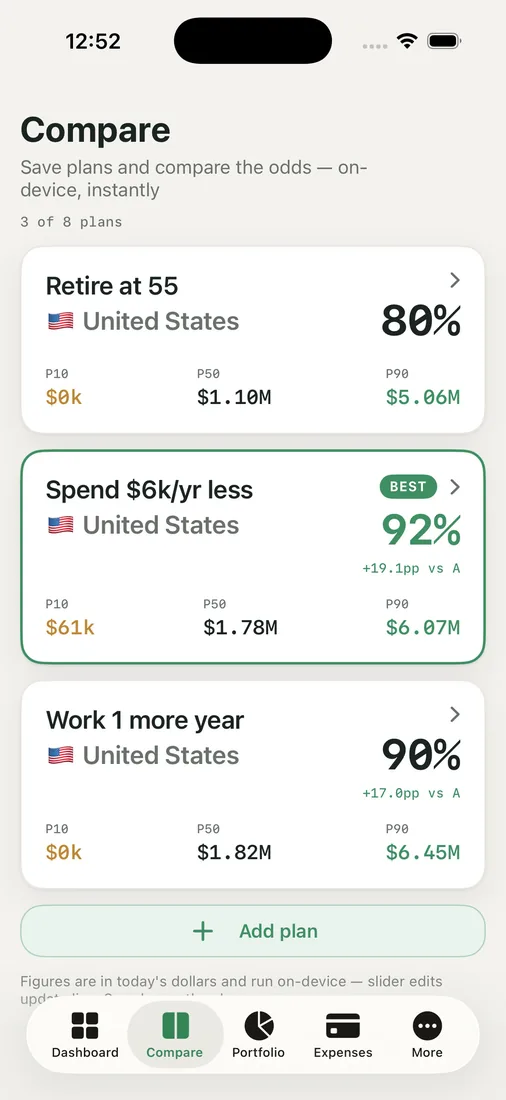

Comparing how to absorb it

A $300,000 spike is big enough that how you absorb it matters as much as whether you can. So we test the options against each other in Compare Plans, each with its own Chance of Success percentage and a "BEST" badge on the front-runner.

We line up a few honest versions: pre-funding college heavily so the spike is smaller when it lands; carrying it from the portfolio as we go; trimming our own retirement spending during the tuition years to soften the blow; and a mixed approach. Each path produces a different number, and the differences are real.

For our numbers, the versions that did some pre-funding and eased our own spending during the overlap years held up best — the load was spread instead of dumped on the most fragile moment. Your numbers will point somewhere else. The value isn't the specific winner; it's seeing the trade-offs priced in odds before you live them.

A $300,000 tuition bill is genuinely a second mortgage. But a second mortgage you've put on the timeline, stress-tested against bad markets, and compared across strategies is a problem you can plan around — not a napkin number that ruins your evening in Valencia.

Key takeaways

- Two kids through college can run near $300,000 — a second-mortgage-sized obligation that arrives in a tight cluster of years, often right at early retirement.

- Unlike a mortgage, tuition hits in big annual lumps with no spreading, so a large withdrawal in a down year can do lasting damage.

- Model each college year as a dated expense in today's dollars so the bill becomes a visible spike on the same timeline as your nest egg.

- Compare ways to absorb it — pre-funding, drawing down, trimming your own spending during the overlap — by their success odds, not gut feel.

Got a tuition bill that looks like a second mortgage? Run your own odds and put it on the timeline with your nest egg.