How Much Does Helping the Kids Delay Retirement?

Generosity has a date attached. We quantified how much paying for college pushes our retirement back.

"We'll figure it out" is what we used to say whenever college came up. It felt generous and brave. Then one evening Mona asked the obvious follow-up: figure out what, exactly, and what does it cost us? We realized we'd been making a six-figure decision on vibes. Generosity feels free in the moment, but it always has a date attached — and for us, that date was our own retirement.

So we stopped hand-waving and put a number on it.

Generosity is a line item

Here's the uncomfortable framing that helped us: paying for your kids' education isn't a separate question from retirement. It's a withdrawal from the same lifetime pool, just earlier and labeled differently. Every dollar of tuition is a dollar that won't be working for you for the next 30 years, plus the growth it would have earned. That compounding loss is the real cost, and it's bigger than the tuition itself.

The honest question isn't "can we afford to help?" It's "how many extra months or years of working does each level of help buy?" Once you frame it that way, generosity becomes something you can dial up or down on purpose instead of stumbling into.

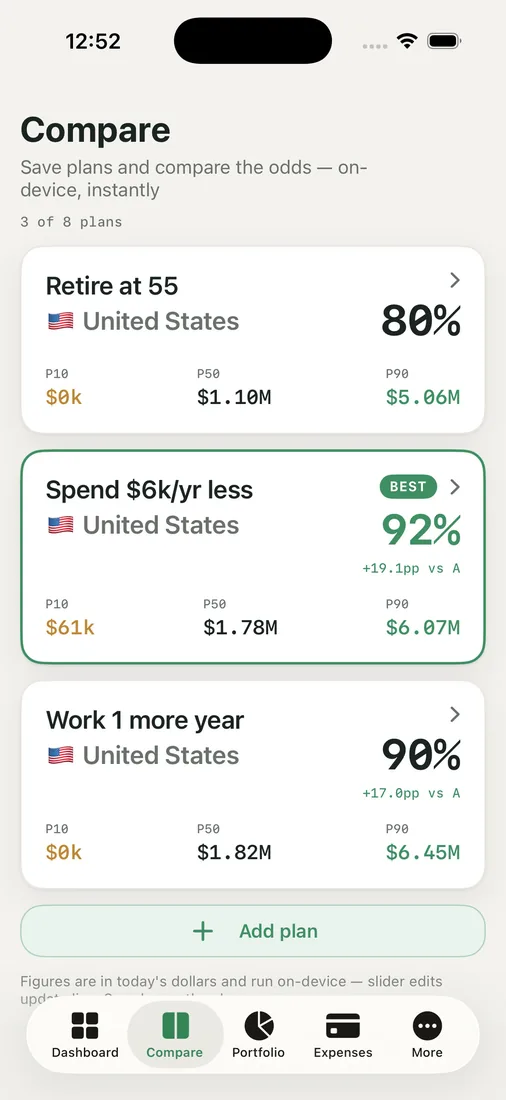

Putting a date on it

We modeled three levels of support in Compare Plans, each as its own scenario:

- Full ride. We cover four years, room and board included, at a private-university cost for both kids.

- Half. We cover roughly half and the kids handle the rest through aid, work, and a cheaper first two years.

- Public floor. We fund a public or European-equivalent path and treat anything beyond that as the kids' problem to solve.

Each scenario came back with a retirement date and a success percentage, and the "BEST" badge landed on the one with the strongest odds. The spread was the eye-opener. Moving from the public floor to the full ride pushed our modeled retirement out by roughly three years and dropped our long-run success odds by a meaningful chunk. The half scenario sat almost exactly in the middle — about a year and a half of extra working, with odds we were comfortable with.

Three years of our lives. That's what "we'll figure it out" actually meant, expressed in the only currency that matters to people chasing early retirement: time.

What we decided to do with the number

Knowing the cost didn't make us stingy. It made us deliberate. We chose something close to the half scenario, because the marginal three-years-of-work for a full ride wasn't a trade we wanted to make — and frankly, we think a kid with some ownership of the cost gets more out of the experience.

The point isn't that you should help less. Plenty of families look at the same screen and happily decide the extra years are worth it. The point is to make the choice with your eyes open, in years and odds, rather than discovering the cost retroactively when you're 58 and wondering why the finish line keeps moving.

We revisit the comparison annually. As the older one's plans firm up — public, private, abroad, gap year — we swap in real numbers and watch our date move. It keeps the decision honest, and it keeps us from quietly mortgaging our own freedom one "we'll figure it out" at a time.

Key takeaways

- College support is a withdrawal from the same pool as retirement, plus decades of lost compounding — so its true cost is measured in years of working, not just tuition.

- Model a few levels of help as separate scenarios and read off the retirement date and success percentage for each; the spread is usually larger than people expect.

- The "half" path often costs surprisingly little extra time while still giving the kids a real education and some ownership.

- Deciding to help is a values call — but make it with the number in front of you, not on vibes.

Want to see what your generosity costs in years? Run your own odds and watch your date move.