College AND Retirement: Can You Do Both?

With kids 14 and 11, tuition and our retirement date collide. Here's how we plan for both at once.

Our 14-year-old starts college in four years. Our 11-year-old follows three years after that. By the worst possible coincidence, the front half of those tuition bills lands right around the early-retirement date we've been working toward for five years. For a while we treated these as two separate problems on two separate spreadsheets — a college fund over here, a retirement plan over there — and quietly hoped they wouldn't notice each other. They noticed. The truth is that college funding and your retirement date pull on the exact same pool of money, and pretending otherwise is how plans go wrong.

Two goals, one wallet

The reason this is hard is simple: every dollar can only do one job. A dollar we put toward college is a dollar not invested for retirement, and vice versa. They draw from the same well and they compete on the same timeline.

What makes it sharper for early retirees is when the costs hit. Traditional retirement at 65 often leaves tuition years safely in the rear-view mirror — the kids are launched before the paychecks stop. Retire in your early fifties with teenagers, and the most expensive years of parenting overlap directly with the first, most fragile years of living off your portfolio.

Those early retirement years are the ones that matter most. A big withdrawal for tuition during a down market, right after you've stopped earning, is precisely the scenario that does lasting damage to a plan. So the collision isn't just inconvenient — it lands at the worst possible moment.

Why one timeline beats two spreadsheets

The fix that changed everything for us was putting both goals on a single timeline. Instead of a college tab and a retirement tab, we model tuition as a set of large, dated expenses sitting right inside the same plan as our retirement spending.

Now the bills aren't a separate worry — they're four (eventually seven) years of elevated outflow that the plan has to absorb, drawn on the same calendar as everything else. We can see the exact years where college and early retirement stack on top of each other, and we can watch what that double-load does to the portfolio in the years it can least afford it.

This is also where the trade-off becomes visible instead of theoretical. Funding college more aggressively might push our retirement date out. Retiring on schedule might mean asking the kids to share more of the cost, or choosing differently on schools. Those are real, values-laden decisions — but at least now they're decisions, made against numbers, rather than a vague unease that we're shortchanging one goal to feed the other.

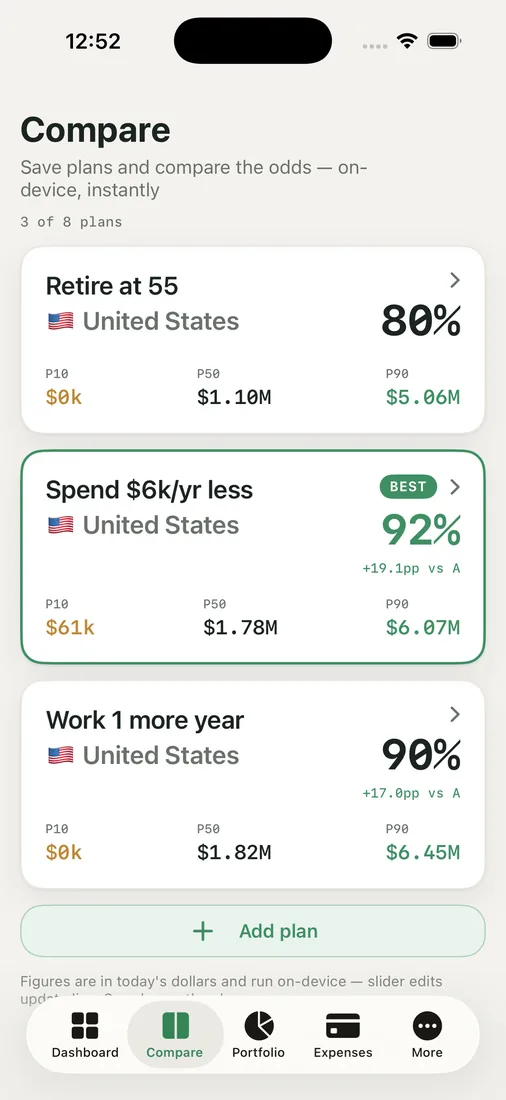

Comparing the paths

Rather than agonize, we build the options and let them compete. In Compare Plans we line up scenarios side by side — one that fully funds college and delays retirement a couple of years, one that retires on time with a leaner college contribution, one that splits the difference — and each carries its own Chance of Success percentage with a "BEST" badge on the strongest.

It doesn't make the choice for us — no tool can decide how much college we want to pay for. But it tells us the price of each path in the only currency that matters here: the odds that the whole plan holds together.

Can a family do both college and early retirement? Often, yes — but rarely both at full throttle, and almost never by accident. The families who manage it are the ones who stop running two plans and start running one, where the bills and the freedom date have to live with each other honestly.

Key takeaways

- College funding and your retirement date draw from the same pool of money — running them as separate plans hides the competition between them.

- For early retirees the timing is brutal: tuition often lands in the first, most fragile years of living off the portfolio, when a big withdrawal does the most damage.

- Put both goals on one timeline so you can see exactly where the costs stack and what they do to the plan in the years it can least afford it.

- Compare funding strategies side by side with their own success odds — it won't decide your values, but it'll price each path honestly.

Wondering whether you can swing both? Run your own odds with college and retirement on the same timeline.