Your Portfolio Is 100% Stocks. Here Are Your Odds.

More equities means more growth and more white-knuckle years. Here's how allocation moves the odds.

For most of our saving years, our portfolio was effectively all stocks, and we wore it like a badge. Mayur would point at the long-run charts: equities win over decades, bonds are for the timid, just hold on. It worked beautifully while we were earning, because a bad year was just a discount on the next purchase. Then we started planning to actually live off the money, and that same all-stock portfolio started to look less like a badge and more like a dare.

Why allocation changes the question

When you're accumulating, volatility is almost a friend — downturns let you buy cheap. When you're spending, volatility flips on you. A big drop early in retirement, while you're pulling money out, can do permanent damage, because shares sold in a crash never get to recover. That's the sequence-of-returns risk that haunts every withdrawal plan.

An all-stock portfolio leans hard into both sides of that bargain:

- Higher expected growth, which raises the ceiling and helps against the slow killer, inflation.

- Much bigger swings, which raises the odds of an ugly stretch landing at exactly the wrong time.

So "100% stocks — am I fine?" doesn't have a one-word answer. More equities genuinely lifts some futures and genuinely sinks others. The only way to know your net result is to look at the full distribution.

Watching allocation move the gauge

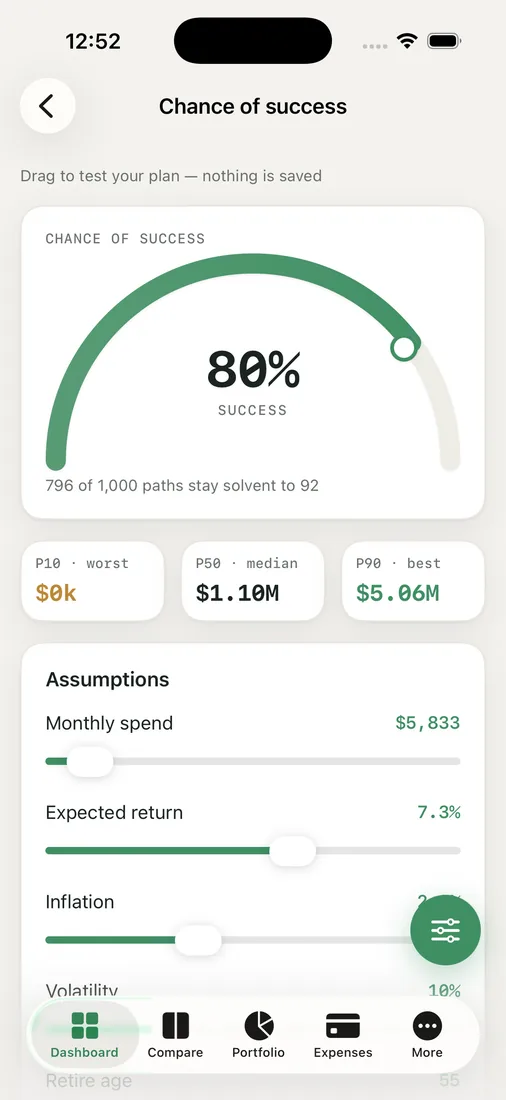

On the Chance of Success screen, we don't argue about allocation in the abstract — we model it. The simulation's return and volatility are anchored to how much equity we hold, so a more aggressive mix shows up as both a higher expected return and a wider spread of outcomes across the 1,000 paths.

What we watch closely is the gap between the P10 and P90 bands. A heavily-stock portfolio stretches that gap wide: the P90 best case gets dazzling, but the P10 worst case gets scarier. The headline success percentage might barely move, while the range of possible lives gets dramatically more dramatic. That spread, not just the average, is what we have to be able to stomach.

Where the donut comes in

We also keep an eye on the Portfolio view, where the allocation donut shows exactly how concentrated we are. Seeing it as a picture made the abstract feel concrete, and it's where we started taking glide-path and bond-tent ideas seriously — gradually dialing back equities around the retirement date to blunt the worst sequences, then drifting back up later.

We haven't talked ourselves out of stocks; we still believe in them. What changed is that we stopped treating "100% equities" as obviously safe or obviously reckless. It's a choice about how much white-knuckle range we're willing to carry, and now we can see the range before we decide.

Key takeaways

- An all-stock portfolio widens your range of outcomes — better best cases, worse worst cases — more than it cleanly raises or lowers your odds.

- The danger in retirement is sequence risk: a big early drop while you're withdrawing can be permanent.

- Watch the P10–P90 spread, not just the headline success percentage.

- A glide path or bond tent around the retirement date can soften the worst sequences without abandoning growth.

See what your allocation does to your range — run your own odds and compare the bands.