Is the 4% Rule Still Safe in 2026?

The 4% rule is a rule of thumb, not a guarantee. Here's what a 1,000-path simulation says about spending 4% today.

The 4% rule showed up in our planning the way it shows up for everyone: as a comforting shortcut. Take your savings, multiply by 4%, and that's what you can spend each year, forever. For a couple at 46 and 43 with two kids and a forty-year horizon ahead, that one number was seductive. It also felt too clean to trust. So we did what we always do now — we tested it instead of believing it.

Where the 4% rule came from

The rule comes from research into US market history. The finding was that a retiree who pulled 4% of their starting balance in year one, then raised that dollar amount with inflation each year after, would have survived every rolling 30-year period in the historical record without going broke.

That's a real, useful result. But notice the fine print baked into it:

- It was built on 30 years, not the forty-plus an early retiree needs.

- It assumed a specific US stock-and-bond mix.

- It describes the worst historical case surviving — not a comfortable margin.

For us, every one of those assumptions wobbles. We're retiring early, we spend across currencies, and "US history" is one possible future, not the only one.

Testing 4% instead of trusting it

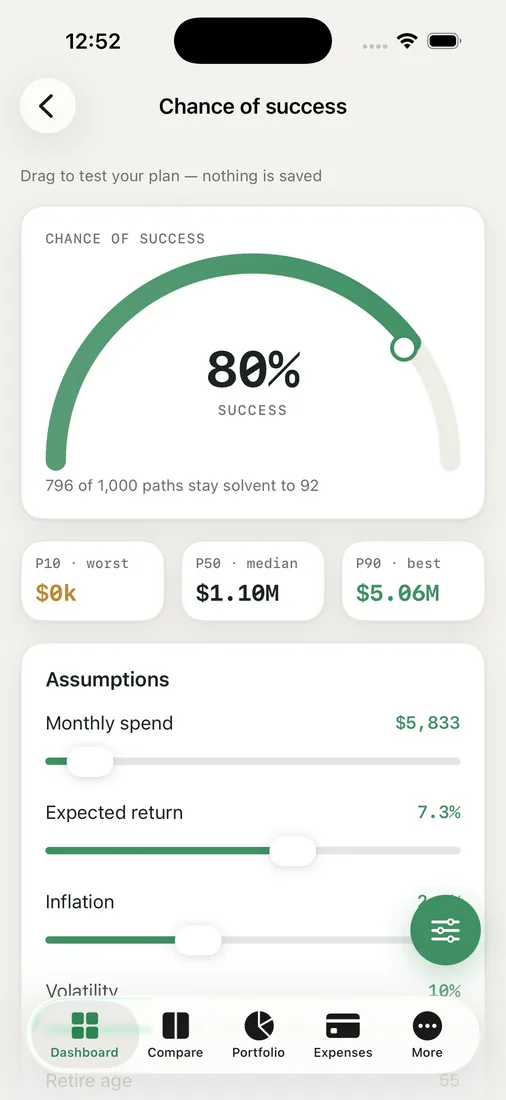

This is exactly what the Chance of Success screen is for. We set spending to 4% of our portfolio and let RetireOdds run 1,000 different futures — each one a different sequence of returns and inflation — and report how many of them the money survived.

The first time we did this, the gauge didn't say "safe" or "unsafe." It gave us a percentage, and then the percentile bands told the fuller story: the P50 path left us with plenty, while the P10 path — the rough worst case — finished uncomfortably thin. That spread is the part the tidy 4% rule hides.

The thing that actually breaks 4%

The villain isn't usually a low average return. It's sequence of returns — getting bad years early. Spending a fixed, inflation-adjusted amount feels disciplined, but if the market drops 30% in your second year of retirement, that rigid withdrawal forces you to sell more shares at the worst possible moment, and the portfolio may never catch up. The random-normal engine, the bootstrap of real US history, and the historical backtest all let us see how often that early-shock scenario shows up.

What we do with the number

Once we could see 4% as a probability rather than a law, two practical moves opened up.

First, we tried a slightly lower starting rate and watched the odds climb — a reminder that small changes in spending move the gauge more than almost anything else. Second, we looked past constant-dollar spending entirely. A flexible approach, where we ease off a little after a bad year, tends to lift the odds without gutting our lifestyle, because it stops forcing sales into a falling market.

Is 4% still safe in 2026? Our honest answer is that it's a reasonable starting point and a terrible stopping point. It's where you begin the question, not where you end it.

Key takeaways

- The 4% rule is a historical rule of thumb built on 30-year US periods, not a guarantee — and especially not for a forty-year early retirement.

- The real danger is sequence of returns: bad years early, paired with rigid spending, are what sink a plan.

- Run your actual spending through a 1,000-path simulation and read the low end, not just the average.

- A little spending flexibility usually buys more safety than reaching for higher returns.

Want to see what 4% looks like for your plan instead of the textbook's? Run your own odds.