$1 Million Sounds Like a Lot. Is It Enough?

A seven-figure balance feels like the finish line. Whether it funds your life is a different question — and the one that counts.

We still remember the day a brokerage balance first crossed a million. It felt like a door opening. Then, almost immediately, a quieter thought walked in behind it: a million what, for whom, lasting how long? We're a family of four — Mayur at 46, Mona at 43, kids at 14 and 11 — who've paid rent in baht, Singapore dollars, and now euros, with college bills lining up like planes on a runway. A million dollars is a wonderful number and a completely useless answer on its own.

Why the balance is the wrong question

"Is $1 million enough" feels like a math problem with one answer. It isn't, because the number doesn't carry any of the things that actually decide the outcome:

- How long it has to last. A million across 25 years is a different animal than a million across 45.

- How much you spend. The same balance is generous at one spending level and dangerous at another.

- What you spend it in. Our costs move with exchange rates; a million in dollars buys a fluctuating amount of European life.

- When the bad years hit. A rough market early on can hollow out a million faster than a slow one ever could.

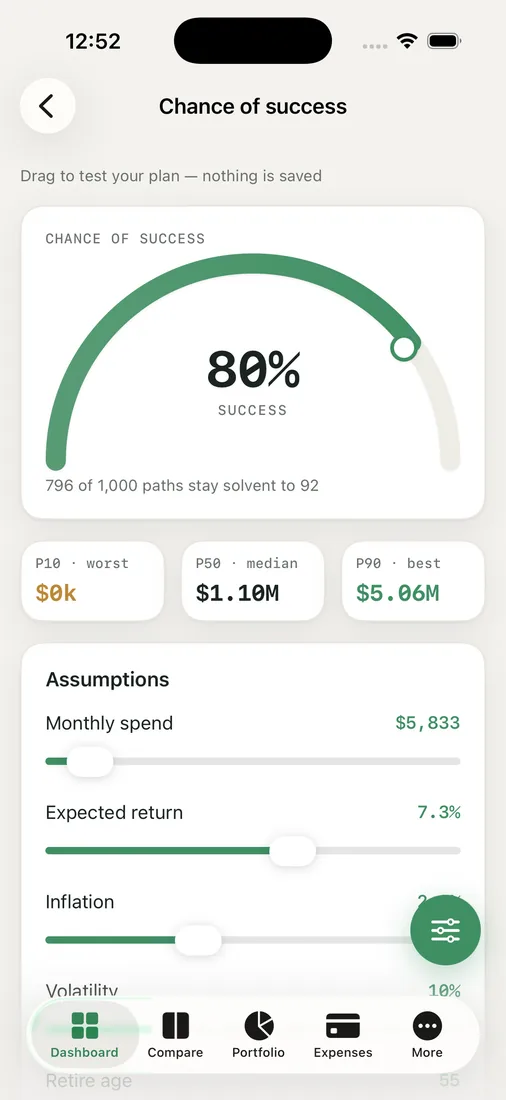

So the better question is the one RetireOdds is built around: given your spending, your timeline, and a thousand possible market futures, in how many of them does this money last?

Turning a million into a probability

We type the balance, our spending, and our ages into the Chance of Success screen and let it run 1,000 simulated futures. Out comes a percentage and a set of percentile bands.

The gauge is the headline, but the bands are where the truth lives. The P50 path shows the median outcome. The P90 path is the happy surprise. The P10 path — the rough worst case — is the one we plan against, because that's the future we'd actually have to survive. Crucially, everything is shown in today's dollars, so a balance decades out doesn't flatter us with inflated digits that buy half as much bread.

The two levers that change the answer

When the first number came back, we didn't argue with it — we played with it. The what-if sliders let us move spending, retire age, return, and inflation and watch the odds respond in real time.

Two levers did almost all the work. Spending was the big one: trimming the annual figure modestly lifted the odds more than any heroic return assumption ever could. The second was time — a slightly later retirement date both shortened the spend-down and stretched the saving, and the gauge noticed.

It also helped to flip between the three engines. If a million only looks "enough" under the most optimistic random-normal run but stumbles when we replay actual US history, that's not enough — that's a coin flip wearing a suit.

The honest verdict for us: a million can absolutely be enough, and it can absolutely fall short, and the only way to know which is to attach it to your real numbers. The balance is the headline. The odds are the story.

Key takeaways

- A balance alone can't tell you if it's enough — spending, time horizon, and currency all change the answer.

- Convert the dollar figure into a probability across many futures, and read the P10 worst case, not just the average.

- Lower spending and a slightly later date usually move the odds far more than chasing higher returns.

- Check the answer across multiple engines; "enough" should hold up under real history, not just the rosy scenario.

See whether your number is actually enough — run your own odds and watch the gauge respond.