A Big Payout: Retire Now or Keep Going?

A seven-figure payout can move your retirement date to today. Whether it should is a simulation, not a feeling.

When Mayur's deferred comp finally paid out, the first thought wasn't joy — it was a question that kept us up: could we just stop now? A seven-figure number has a way of whispering that the finish line is right here, today. The trouble is that the whisper is a feeling, and a 40-year retirement can't be run on a feeling. It has to be run on a simulation.

So before anyone handed in any notice, we did what we always do: we turned the question into two plans and made them argue with each other.

The seductive math

A big payout can genuinely move your retirement date to today. Add a large lump sum to the portfolio, divide by a safe withdrawal rate, and if the answer covers your spending, you're technically done. That arithmetic is real, and it's intoxicating.

But it hides two things that matter enormously for early retirees.

First, a few more years of work do double duty. Each year you keep going adds savings and removes a year the portfolio has to fund. That's a powerful one-two punch on your odds — often more powerful than the payout itself.

Second, the payout is exposed to bad timing. If you retire the day the money lands and the market drops 20% the following year, you're selling into the decline to live on. That sequence-of-returns risk is the single biggest threat to a long retirement, and "retire now" walks straight into it with the whole windfall.

The feeling says stop. The simulation asks: stop into what?

Making the two futures argue

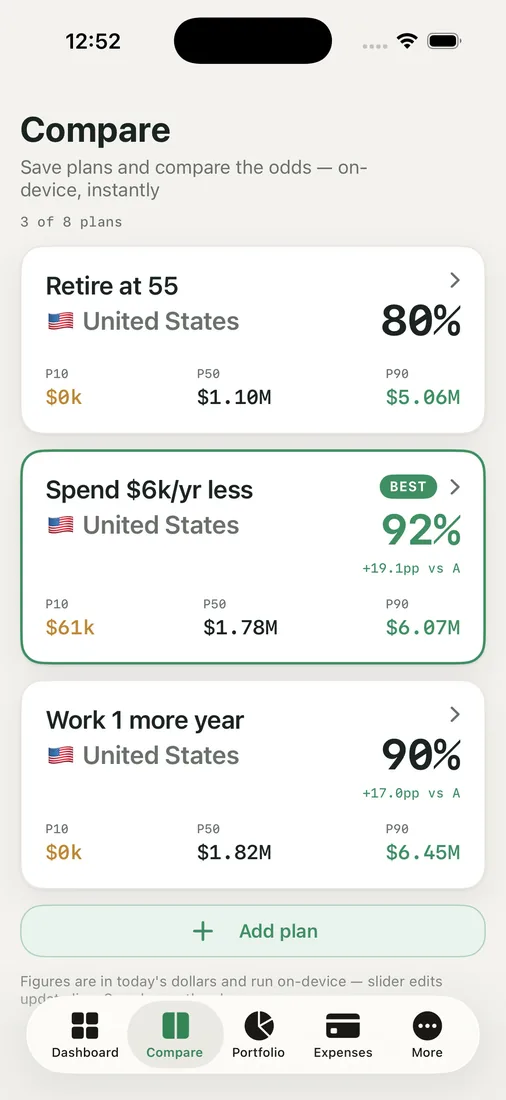

We built both versions in Compare Plans.

- Retire now — add the after-tax payout to the portfolio and stop working today.

- Keep going — bank the payout and work two more years before pulling the plug.

Each scenario returned its own success percentage and a "BEST" badge on the stronger one. What surprised us was how close they were. "Retire now" already cleared a healthy margin — the payout really had done most of the work. The extra two years bought a few more points of safety and a fatter cushion, but not a different life.

That's the moment the decision stops being scary. When both futures are survivable and you can see the exact price of each, you're no longer gambling. You're choosing between two good outcomes, with the cost of each one printed on the screen.

We didn't trust the gauge alone

A single success percentage is a headline, not a verdict. We took the "retire now" plan into Chance of Success and ran the 1,000-path Monte Carlo, then looked past the median to the P10 — the unlucky-market path. If even the gloomy path keeps us fed and housed, the plan is robust. If only the median survives, the payout is funding a hope, not a retirement.

We also nudged the what-if sliders: a worse return assumption, a higher spend, an early bad decade. The plan held. That's what gave us the confidence the gauge alone couldn't.

In the end we chose a soft version of "keep going" — one more year, mostly to smooth the kids' college overlap — not because "retire now" failed, but because we could see it cost us almost nothing and bought real peace of mind.

Key takeaways

- A big payout can mathematically move your retirement to today, but the arithmetic hides sequence-of-returns risk and the double benefit of a few more working years.

- Build "retire now" and "keep going" as side-by-side scenarios and read the success percentage on each — the gap is often smaller and clearer than the feeling suggests.

- Don't trust a single number: run the winning plan through a Monte Carlo and judge it by the unlucky-market path, not the median.

- When both futures are survivable, the decision becomes a values choice with a visible price tag — which is a far better place to stand than a gut feeling.

Sitting on a payout and wondering if you're done? Run your own odds and let the two futures argue it out.