Don't Blow the Windfall: The Tax on the Sale

The headline number isn't what you keep. Capital-gains tax on a big sale can take a quarter of it.

When we sold a chunk of long-held stock to rebalance before a move, the brokerage screen showed a satisfying six-figure number. Then we ran the tax on it and watched roughly a quarter evaporate. The lesson stuck: the headline number on a big sale is not what you keep. It's the number before the government's cut, and that cut can be larger and more avoidable than most people assume.

Windfalls get blown in two ways. The loud way is spending it. The quiet way — the one that gets responsible people — is mishandling the tax on the way out.

The gap between the screen and your bank account

A big sale of appreciated assets triggers capital-gains tax on the profit. How much depends on how long you held it, how big the gain is, and what other income you have that year. Stack a large gain on top of a normal income year and you can push part of it into a higher bracket — paying more than you would have if you'd spread it out.

There's a second, sneakier cost. A spike in income for one year can quietly raise other things tied to your income: in the US, that includes Medicare premium surcharges (IRMAA) years down the line, and for expats it can interact with foreign tax rules in ways that surprise you. The sale doesn't just cost you the gains tax — it can ripple into bills you didn't see coming.

The point isn't that tax is bad. It's that the timing and sequencing of a big sale are levers, and most people pull them by accident.

Seeing the real number first

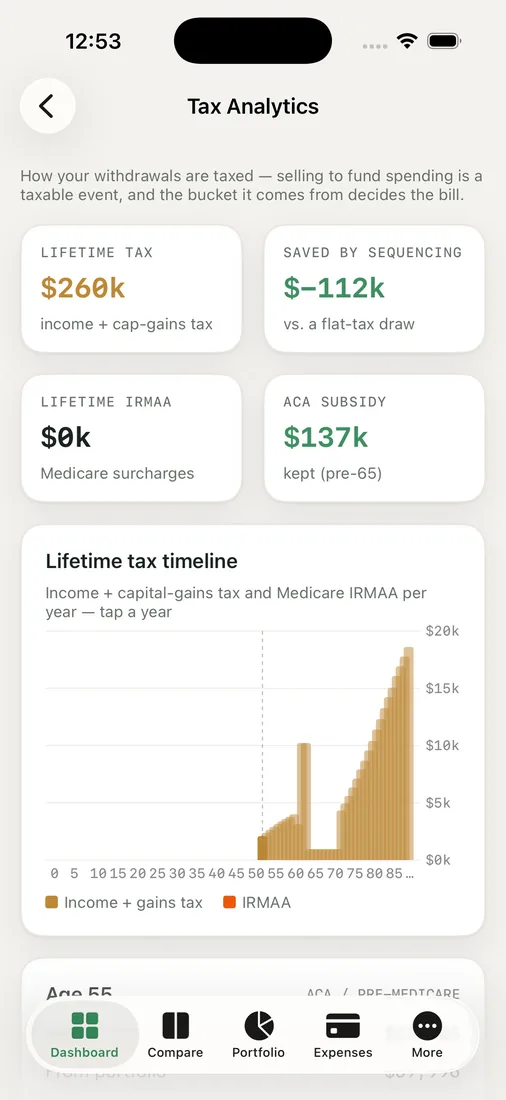

Before we did anything, we modeled the sale in Tax Analytics to see the after-tax proceeds — the number that actually lands in our account, not the one on the brokerage screen.

That alone changes decisions. A windfall that looks like it crosses your retirement line might not, once a quarter of it is gone. Far better to learn that on a screen than after you've already handed in your notice.

The lever almost nobody pulls

The most useful thing the tax view showed us was sequencing. Selling everything in one tax year often isn't the cheapest path. Spreading the sale across two or three years — or harvesting gains in a lower-income year, like the first year after you stop working — can shrink the total tax meaningfully. RetireOdds even surfaces a "saved by sequencing" figure so you can see the difference in plain dollars.

For us, splitting a sale across the calendar boundary and the gap year before a move kept a chunk of the gain in a lower band. That saved money was real — enough to matter to our timeline, not a rounding error.

A few principles we now follow with any large sale:

- Know the after-tax number before you plan around it. The headline is a draft; the net is the truth.

- Spread gains into low-income years where you can. Early retirement creates natural low-income windows — use them.

- Watch the ripple effects, not just the headline rate. Premium surcharges, brackets, and cross-border quirks all key off that one big number.

We treat the tax on a sale as a design problem now, not a bill that shows up later. Sequenced on purpose, the same windfall keeps more of itself.

Key takeaways

- The headline sale price isn't what you keep — capital-gains tax can take a quarter or more, so plan around the after-tax number.

- A one-year income spike can ripple into higher brackets and downstream costs like premium surcharges; the gains tax isn't the only bill.

- Sequencing matters: spreading a sale across tax years or into low-income windows can meaningfully cut the total — the "saved by sequencing" number makes it concrete.

- Model the sale before you act on it, so a windfall that looks like it clears your line actually does once tax is subtracted.

About to sell something big? Run your own odds and see the real number before the tax takes its share.