Your IPO Just Hit. Now What?

A liquidity event changes everything — and nothing, until you run it through the plan. Here's our checklist.

A friend of ours watched the company he'd given six years to finally go public. On paper, his vested shares were suddenly worth more than he'd earned in his whole career. He called us that night, equal parts elated and paralyzed, asking the question everyone asks at that moment: now what? The number on the screen felt like an answer, but it was actually just a new and much louder version of the question.

We've never had an IPO ourselves, but we've spent five years modeling our own freedom date, and we told him what we'd do: nothing irreversible, until the number goes through the plan.

Why the headline number lies

A liquidity event changes everything and nothing at the same time. Everything, because the raw figure is life-altering. Nothing, because almost none of that figure is actually yours yet, and almost none of it is safe where it sits.

Three things stand between the headline and reality:

- Tax. A big sale triggers capital-gains tax — and if you're exercising options, possibly ordinary income and a brutal AMT surprise. The after-tax number can be a quarter to a half smaller than the headline.

- Concentration. Right after the event, your entire net worth is one ticker. The company that made you rich can also un-make you. Single-stock risk is the silent killer of paper fortunes.

- Lockups and volatility. You often can't sell for months, and the price you see on listing day is rarely the price you get.

Until you've subtracted tax, diversified the concentration, and stress-tested what's left, the headline number is a mirage. It tells you something happened. It doesn't tell you whether you're done.

Our checklist before touching anything

We walked our friend through the sequence we'd follow.

1. Model the after-tax number, not the headline

In Tax Analytics, drop in the sale and let it estimate the capital-gains tax so you're planning around what you actually keep. The "saved by sequencing" view also shows whether spreading sales across tax years beats dumping everything in one.

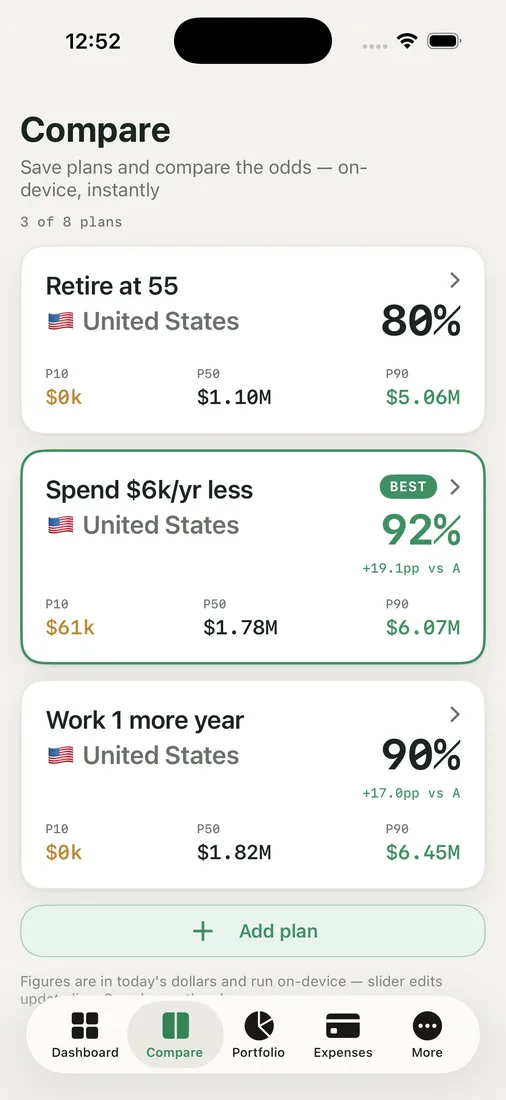

2. Run "retire now" against "keep going"

This is the big one. In Compare Plans, build two scenarios side by side — retire today on the after-tax proceeds, versus bank the windfall and keep working a couple more years.

Each comes back with a success percentage and a "BEST" badge. The point isn't to be told what to do; it's to see whether the windfall genuinely crosses the finish line or just brings it into view. For our friend, "retire now" already cleared a comfortable margin — which is a very different feeling from assuming it did.

3. Pressure-test the survivor

The plan that wins on paper still has to survive a 30- or 40-year horizon. We'd take the winning scenario into Chance of Success and run the 1,000-path Monte Carlo, watching the P10 (the unlucky-market case) as closely as the median. A windfall that only works in good markets isn't a retirement; it's a bet.

The mindset that keeps it

The hardest part isn't the math — it's the patience. A windfall feels urgent and permanent, and both feelings push you toward bad, fast decisions. Our advice was the same we give ourselves: park it somewhere boring, diversify out of the single stock on a schedule, and let the plan, not the adrenaline, set the pace.

Key takeaways

- The headline figure isn't yours — subtract capital-gains and option taxes first, then plan around the after-tax number.

- Right after an IPO your whole net worth is one stock; diversifying out of that concentration is risk management, not pessimism.

- Compare "retire now" against "keep going" side by side so you can see whether the windfall actually crosses the line or just moves it closer.

- Take the winning plan through a Monte Carlo run and watch the unlucky-market path — a windfall that only survives good markets isn't a finished plan.

Just had a liquidity event? Run your own odds before you make a single irreversible move.