Can Social Security Follow You Overseas?

Yes, mostly — but with rules. How we model Social Security as expats living outside the US.

The question came up at a dinner in Singapore, the way these things always do. A friend asked whether we'd lose our Social Security by living abroad. We didn't actually know. We'd paid into the US system for twenty-plus years, but we'd been outside the country for nearly a decade, and we'd half-assumed that benefit was something you collected from a recliner in Florida, not a flat in Spain. It turns out the answer is "yes, mostly — but with rules," and those rules quietly change how we model the next thirty years.

The short, honest version

For US citizens, Social Security generally keeps paying you no matter where in the world you live. The check follows you. There are exceptions — a short list of countries the US won't send payments to, and different treatment for non-citizens — but for an American family abroad, the benefit usually travels.

What changes overseas isn't whether you get paid. It's the texture around it: how taxes work between your two countries, how the money lands in a foreign account, and what it's actually worth once it's converted into the currency you spend. None of that is exotic, but all of it matters for a plan.

This is education, not advice — the specifics depend on your citizenship, your country, and any tax treaty between them, and those are worth checking with a professional. What we can do is show how we model it so we're not flying blind.

The currency problem nobody mentions

Here's the thing that tripped us up. Social Security is paid in US dollars and adjusted for US inflation. But we spend most of our year in euros. So our benefit is a dollar-denominated income stream funding a partly euro-denominated life.

When the dollar is strong, that benefit stretches further in Valencia. When it's weak, it buys less. The benefit amount on the statement never changes, but its real purchasing power in our actual life swings with the exchange rate. A plan that treats it as a flat, reliable floor is missing half the picture.

So we model Social Security as what it is: a dollar income that we then have to spend across currencies. That's exactly the kind of mismatch the dual-currency overlay is built for — income in one currency, expenses in another, with the gap made visible instead of assumed away.

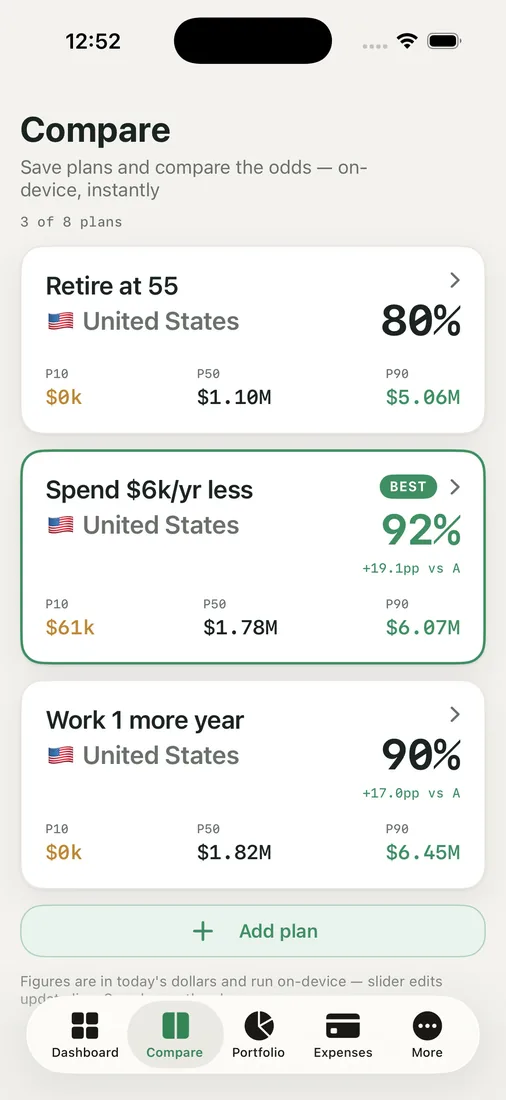

Modeling the "claim early or late" question

The other big lever is when we claim. Claiming earlier gives us a smaller monthly benefit for more years; waiting gives us a larger one for fewer. For most people there's no universally right answer — it depends on health, other income, and how much you value a guaranteed floor later in life.

Rather than argue about it in the abstract, we build it as scenarios. In Compare Plans, we set up one version that claims early and one that claims later, leave everything else identical, and let each one carry its own Chance of Success percentage. The tool puts a "BEST" badge on whichever comes out ahead for our particular numbers — and just as usefully, it shows us when the two are close enough that the decision is really about peace of mind, not math.

Where it fits in the bigger plan

For us, Social Security isn't the star of the plan — it's a backstop that kicks in well after our early-retirement date. But backstops matter most in the bad years, the ones the Monte Carlo's P10 path is built to expose. A modest, inflation-adjusted income arriving in our sixties can be the difference between a rough decade and a ruined one.

So we model it carefully: the right benefit, claimed at a chosen age, paid in dollars, spent across currencies, and stress-tested as part of the whole. The recliner-in-Florida assumption was wrong. The benefit can absolutely follow us overseas — we just have to plan for the journey it takes to get spent.

Key takeaways

- For US citizens, Social Security generally pays you wherever you live, with a few country and non-citizen exceptions — but tax and currency treatment change overseas.

- A dollar-denominated benefit funding a foreign-currency life swings in real value with the exchange rate; model it as income in one currency, spending in another.

- Treat "claim early vs. late" as side-by-side scenarios with their own success odds, not an abstract debate — and notice when they're close enough that it's a comfort decision.

- A modest inflation-adjusted income later in life matters most in the bad-luck paths, so stress-test it as part of the whole plan.

Curious how a delayed claim or a weaker dollar moves your floor? Run your own odds and watch it play out.