Geo-Arbitrage: Cut Expenses, Retire Years Earlier

Lowering your cost of living abroad can shrink your retirement number — and pull your date years closer.

When we lived in Chiang Mai, our family of four spent on rent, food, and a couple of part-time helpers what a single modest apartment would have cost us back in the US. That wasn't deprivation — it was a comfortable life, with a pool, eating out often, and travel. The arithmetic was almost startling: the same lifestyle cost a fraction of the dollars. That's geo-arbitrage, and it does something no investment return can match. It doesn't just stretch your money — it shrinks the finish line.

Why lower spending pulls the date forward

Most retirement math runs in one direction: how big a portfolio do you need to fund your spending? The common shorthand is roughly 25 times your annual expenses. The hidden power in that formula is that it cuts both ways. Drop your annual spending and you don't just need 25 times a smaller number — the gap between what you have and what you need closes from both ends.

Say a family needs $80,000 a year and therefore targets about $2 million. Move somewhere the same life costs $50,000 and the target drops to roughly $1.25 million. That's not a rounding difference — it's hundreds of thousands of dollars you no longer have to accumulate, which can translate into retiring years sooner.

The catch: it's not just rent

The seductive version of geo-arbitrage compares rent and street food and stops there. The honest version counts everything. Cheaper housing and daily life are real, but you have to add back the things that don't get cheaper — and sometimes get more expensive — when you move abroad.

Healthcare is the big one before Medicare age; private international cover is its own line item. There are visa costs, flights home, international school if your kids need it, and the local tax bill on top of the US tax that follows you everywhere. We've seen a "cheap" country turn out merely average once schooling and insurance for two kids were in the total.

And there's the currency layer. A low cost of living in local terms can drift if the dollar weakens against your spending currency, so the bargain isn't fixed.

Modeling the whole trade

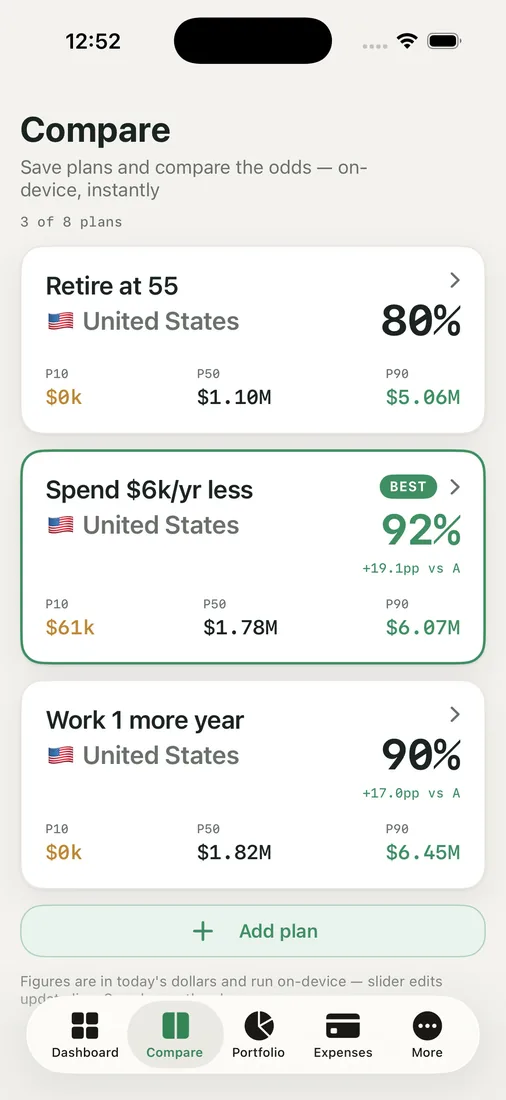

This is precisely why we don't eyeball it. In RetireOdds, the Compare Plans view lets us put real, complete scenarios side by side — Thailand, Spain, and staying put — each with its own cost of living, currency, expat settings, and the full set of add-back costs, all running through the same success engine.

The output that matters isn't just "cheaper." It's two things at once: a smaller required number and an earlier date with the same or better odds of success. Watching our retirement date jump forward by years when we modeled a lower-cost country honestly — schooling and insurance included — is the single most motivating thing we've seen in our own plan.

The Expenses tracker feeds this with the multi-currency reality of how we actually spend, so the cost-of-living numbers in the comparison aren't guesses — they're our life. As always, this is education rather than advice; visa rules and cross-border tax deserve a professional's eye before you commit.

Key takeaways

- Because the target portfolio scales with spending, cutting your cost of living shrinks the number you need and pulls your retirement date earlier.

- The real saving counts everything — healthcare, schooling, visas, flights, and local tax — not just rent and food.

- US tax still follows you, and a weak dollar can erode the local bargain, so model the full picture.

- The payoff to measure isn't "cheaper" but a smaller number plus an earlier date at the same odds of success.

See how many years a lower cost of living could buy you — run your own odds and compare your current city against a cheaper one.