Healthcare Abroad vs. Medicare at Home

Private cover overseas vs. waiting for Medicare — how we compare the true cost across countries.

When Mona needed a minor procedure in Bangkok, the all-in price — excellent hospital, no waiting — was less than what the deductible alone would have been on a US plan. That experience reframed a question that quietly haunts every early retiree: what do we do about healthcare in the long gap before Medicare? For us, retiring in our forties and fifties, that's potentially twenty years to cover before age 65, and the answer turned out to depend enormously on which country we're standing in.

The pre-65 bridge is the scary part

In the US, Medicare doesn't start until 65. Retire before that and you're on your own for the bridge — and that bridge is where a lot of early-retirement plans quietly break.

The domestic option is an ACA marketplace plan. The crucial, often-missed detail is that ACA subsidies are driven by your MAGI — your modified adjusted gross income. Keep your reported income modest and the subsidy can be generous; let it rise and the subsidy shrinks. There's even a cliff in some years where one extra dollar of income costs you the subsidy entirely. That makes US early-retirement healthcare a tax problem as much as a medical one, because the same Roth conversion or capital-gain harvest that's smart for taxes can be expensive for premiums.

What "abroad" changes

Living overseas rewrites the bridge. In many countries, private international health insurance for a family costs a fraction of an unsubsidized US plan, and the out-of-pocket prices — like Mona's procedure — are dramatically lower. For some families, paying cash plus a catastrophic policy is genuinely cheaper than the US system even with a subsidy.

But it's not a clean win everywhere, and the details matter:

- Premiums climb with age, and some international policies get hard to renew or expensive in your later years.

- Coverage back in the US is usually excluded, which matters if you plan to spend time at home.

- A serious, chronic condition can change the calculus entirely and may make the predictability of a home system worth more.

And at 65, Medicare reappears as an option — but only really useful if you're in the US to use it, and skipping Part B while abroad can mean lifelong penalties if you enroll late. Plus IRMAA: high income raises Medicare premiums through surcharges, so the tax-and-healthcare link doesn't end at 65, it just changes shape.

How we actually compare it

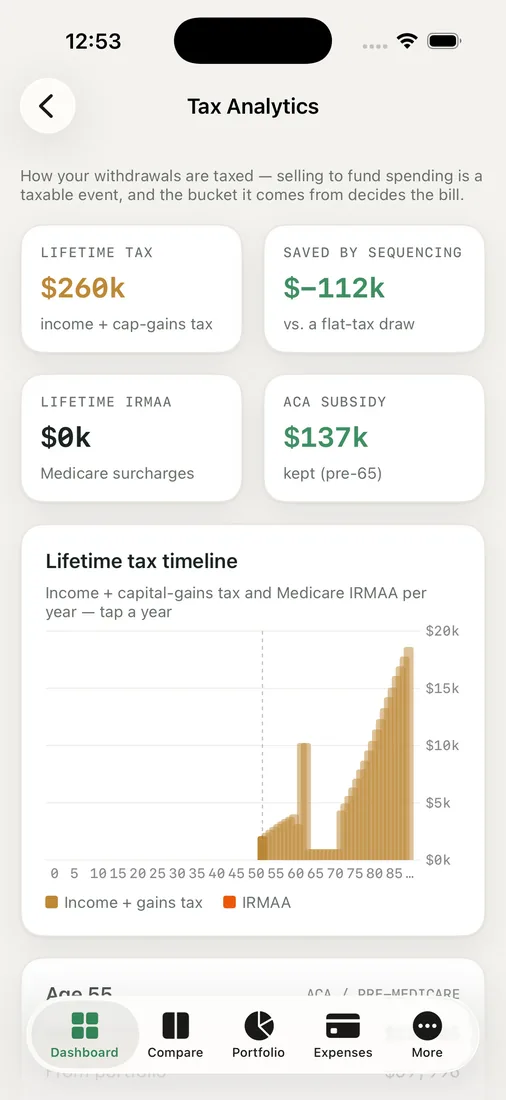

Because the answer is so country-dependent and so entangled with taxes, we don't compare healthcare on its own — we compare whole lives. In RetireOdds, the Tax Analytics view models the pieces that bind healthcare to income: the ACA subsidy and its cliff, and the IRMAA surcharges later, all driven by the MAGI our withdrawal plan produces. So we can see how a conversion decision ripples into our premiums, not just our tax.

Alongside that, the Compare Plans view lets us line up the genuinely different scenarios — Spain with private cover, Thailand with cash-plus-catastrophic, the US on a subsidy-optimized ACA plan — each carrying its real healthcare cost into the same success engine. The winner on premiums isn't always the winner on the bottom line once taxes and the subsidy are in the same picture.

This is one of the most personal and most professional-dependent areas in all of retirement planning, so treat everything here as education, not advice. Insurance terms, treaty details, and Medicare enrollment rules deserve an expert — our aim is to walk in with the right questions and a number we trust.

Key takeaways

- The pre-65 bridge is the hardest healthcare stretch for early retirees, and it can make or break a plan.

- In the US, ACA subsidies depend on your MAGI, so income planning and healthcare cost are inseparable — watch the subsidy cliff.

- Abroad, private cover and cash prices can be far cheaper, but mind renewability, age-based premium climbs, and US-coverage gaps.

- Compare whole scenarios, because the cheapest premium isn't always the best outcome once taxes, subsidies, and IRMAA are included.

See how your healthcare choice and your tax plan move together — run your own odds and compare covering the bridge at home versus abroad.