Retiring Abroad on a US Portfolio

We've lived in Thailand, Singapore and Spain. Here's how a US portfolio actually funds a life overseas.

Our accounts are in dollars. Our rent, in the last few years, has been in baht, then Singapore dollars, now euros. That single mismatch — earn in one currency, live in another — is the whole story of retiring abroad on a US portfolio, and it's the reason every calculator we tried before building our own felt like it was answering a different family's question.

The good news we learned by living it: a US portfolio can absolutely fund a life overseas. But you have to plan it as a cross-border problem from day one, not as a domestic plan with a plane ticket stapled on.

The portfolio stays American. The tax follows you.

Here's the part that surprises people most. Moving abroad doesn't move your money. Our brokerage and retirement accounts stay in the US, invested in the same funds, growing in dollars. What changes is where we spend the withdrawals.

And critically, US federal tax follows you around the world. America taxes its citizens on worldwide income no matter where they live. So even sitting in Spain, we still file a US return and still owe US tax on portfolio withdrawals, dividends, and gains. What often doesn't follow you is state tax — leave a state behind properly and that layer can fall away. That alone can be worth real money.

The second tax bill

The complication is that the country you live in may also want to tax you. Spain taxes residents on worldwide income; Thailand and Singapore have their own rules; treaties change the details everywhere. The fear is obvious: get taxed twice on the same dollar.

The main tool against that is the Foreign Tax Credit. In broad terms, tax you pay to your country of residence can offset the US tax on the same income, so you're not paying both governments in full on the same dollar. It's not automatic and it's not perfect — the categories and timing get intricate — but it's the mechanism that keeps a cross-border plan from being crushed by double taxation. This is firmly the territory where you confirm the specifics with a cross-border professional; our job is to ask the right questions.

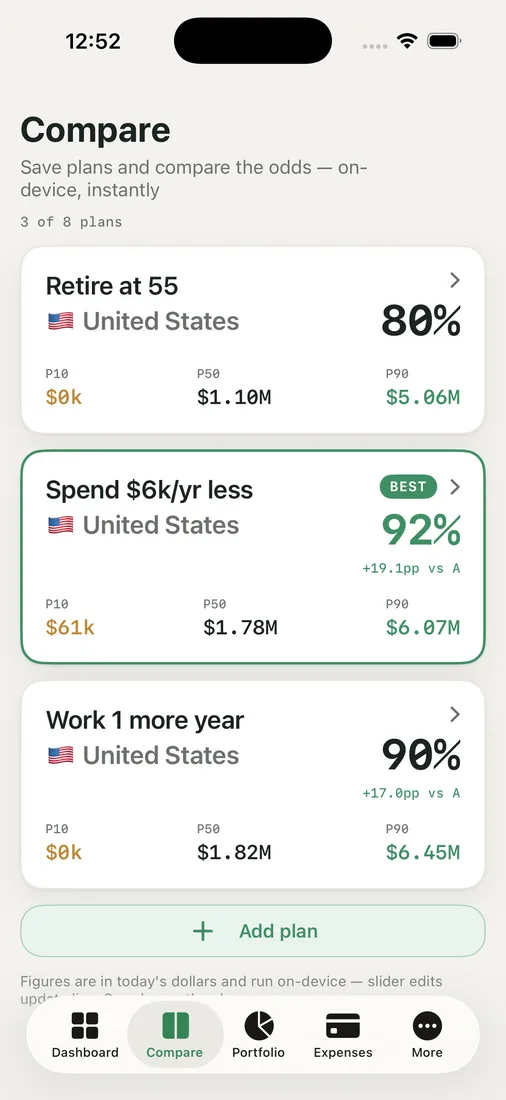

Why we compare countries side by side

The hardest part of all this is that "can we afford to retire abroad?" has a different answer in every country, because the spending currency, the cost of living, the local tax, and the healthcare cost are all different.

So we stopped trying to hold it in our heads and built it into RetireOdds. The Compare Plans view lets us put scenarios next to each other — Spain versus Singapore versus staying in the US — each with its own country and expat settings, its own currency, and its own assumptions, all feeding the same success-rate engine. Seeing three columns with three different odds of success is what turned a vague dream into a decision.

Underneath, the expat tooling carries a dual-currency overlay, so we can watch a withdrawal in dollars and what it actually buys in euros at the same time, and an Expenses tracker that already speaks several currencies because that's how our real spending arrives.

What we'd tell our younger selves

Three things. First, the portfolio is the easy part — keep it simple and in the US. Second, the tax is the hard part, it's two-country, and it rewards planning years ahead of the move. Third, the answer is country-specific, so model the actual place, not a generic "abroad." None of this is advice — cross-border tax genuinely needs a professional — but with the right questions in hand, that conversation is far cheaper and far more useful.

Key takeaways

- A US portfolio can fund life overseas, but you must plan it as a two-country problem from the start.

- US federal tax follows citizens worldwide; state tax often does not, which can save real money.

- The Foreign Tax Credit is the main defense against being taxed twice on the same income — confirm the details with a cross-border professional.

- "Can we afford it?" is country-specific, so compare actual destinations side by side rather than planning for a generic "abroad."

See whether your US portfolio funds the life you're picturing overseas — run your own odds and compare the countries you're considering.