Early-Retirement Health Insurance: The Real Cost

Before Medicare, your income decides your premium via ACA subsidies. Here's how we keep ours affordable.

When we got our first real quote for a US family marketplace plan without an employer behind it, the number made Mayur put the laptop down and go for a walk. A family of four, no subsidy, can face premiums that rival a mortgage payment. But here is the twist we did not understand at first: that scary sticker price is not necessarily what you pay. In early retirement, before Medicare, your health insurance bill is largely a function of one number you partly control, your income.

The rule that changes everything

The Affordable Care Act offers premium subsidies that lower what you actually pay for a marketplace plan. The size of the subsidy depends on your modified adjusted gross income, or MAGI, relative to certain benchmarks. Lower reported income, bigger subsidy, smaller premium. Higher reported income, smaller subsidy, bigger premium.

Read that again, because it is the whole game. The marketplace does not look at your net worth. It looks at the income you report for the year. An early-retired family living comfortably off a large portfolio can show modest taxable income, and that modest income can unlock real subsidies.

So a wealthy retiree and a working family with the same income can pay similar premiums, even though their balance sheets look nothing alike. For people who have saved hard and can choose how they draw down, that is a genuine lever.

The cliff at the edge of the lever

There is a catch that has earned the nickname the ACA cliff. Subsidies phase out as income rises, and in some years and rules, they can fall off sharply past a threshold. Cross it by a little and you can lose a large subsidy all at once, turning an affordable plan back into that mortgage-sized bill.

That makes early-retirement health insurance a precision exercise, not a set-and-forget. The same income moves we use for tax planning, Roth conversions, harvesting gains, choosing which account to spend from, all push our MAGI up or down, and therefore push our premium up or down.

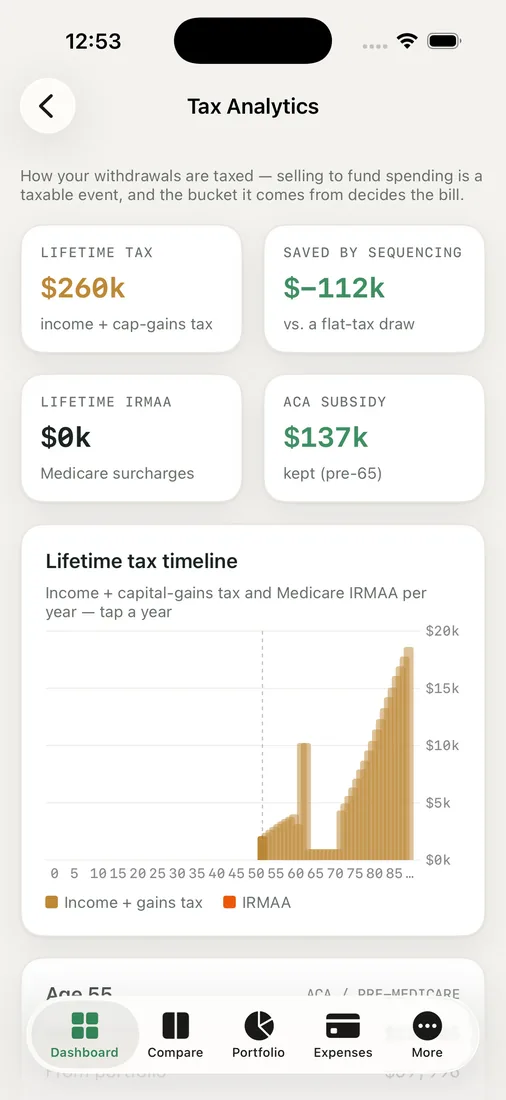

The tax and healthcare view in RetireOdds is where we keep this honest. We can see our projected MAGI for each pre-65 year, where the subsidy bands and the cliff sit, and what a planned conversion or withdrawal does to the premium we would actually pay. It connects two things that most tools keep in separate rooms: how we fund our spending and what our health coverage costs.

How we keep ours affordable

Our approach, shared as illustration and not advice, comes down to managing reported income across the bridge years.

- We lean on a mix of sources, taxable, Roth, and cash, so we can hit a target reported income rather than letting it land wherever it falls.

- We size any Roth conversions to fill space under the relevant threshold instead of spilling over the cliff.

- We watch the years where a big realized gain or distribution would spike MAGI and, where we can, spread those moves out.

There is also our wildcard, geography. We have lived in Thailand, Singapore, and Spain, and for part of our pre-Medicare window we may not be buying US coverage at all. Out-of-pocket care in some places, or local coverage, can cost a fraction of the US marketplace. That option does not erase the planning, it just gives us another dial, and it is one more reason a calculator that ignores where you live was never going to work for us.

We are not steering you toward any particular income target, and the rules shift over time. The point is that pre-Medicare health insurance is one of the few big retirement costs you can actively shape, if you plan your income with the premium in mind.

Key takeaways

- Before Medicare, ACA premium subsidies are driven by your reported income, not your net worth, so disciplined drawdown can unlock real savings.

- The ACA cliff means crossing an income threshold can cost you a large subsidy all at once, so precision matters.

- The same moves you use for tax planning move your premium too, which is why income and healthcare should be planned together.

- Living abroad for part of the bridge can change the cost entirely and gives you another lever.

If you are heading into the years before Medicare, it is worth seeing how your income choices move your premium. Run your own odds and find the income target that keeps your coverage affordable.