IRMAA: The Medicare Surcharge That Ambushes High Earners

A single dollar over a threshold can raise your Medicare premiums for a whole year. We watch the cliffs.

We learned the word IRMAA the way most people do: from someone older and wealthier than us, fuming. A friend in his late sixties had done one large Roth conversion in a strong market year, felt clever about it, and then discovered his Medicare premiums had jumped for the following year because that conversion pushed his income one notch too high. He had crossed an invisible line by a few thousand dollars and paid for it twelve months straight. Mayur is only 46, but that story stuck, because it is precisely the kind of trap we are trying to design around now.

What IRMAA actually is

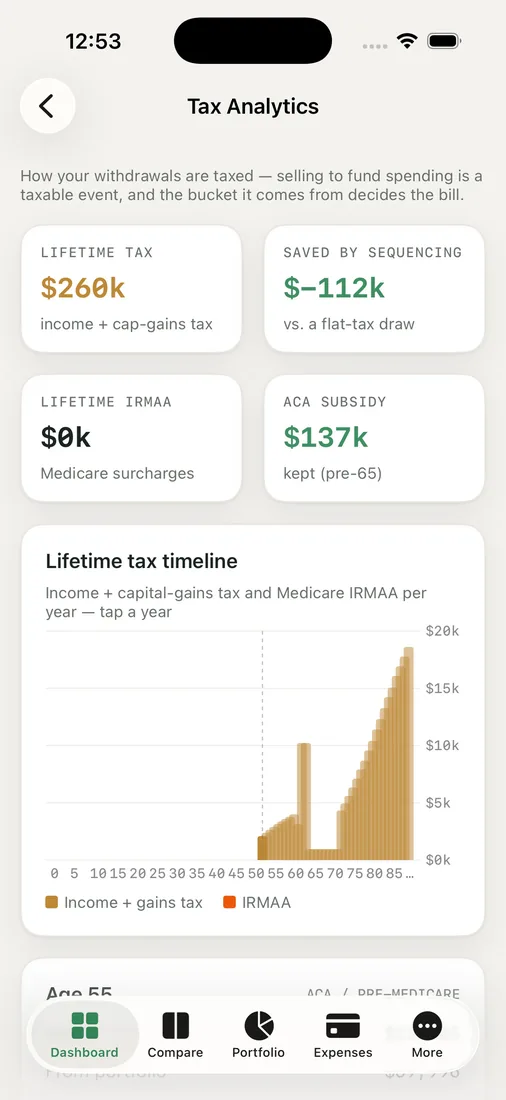

IRMAA stands for the Income-Related Monthly Adjustment Amount. In plain English, it is a surcharge on your Medicare Part B and Part D premiums that applies once your income climbs above certain thresholds. Below the line, you pay the standard premium. Above it, you pay more, and the more you earn, the more the surcharge climbs through several brackets.

Two details make IRMAA sneaky.

First, it is a cliff, not a ramp. Go one dollar over a threshold and you do not pay a little more, you jump to the whole next surcharge tier. A trivial overage can cost a meaningful amount for the entire year.

Second, it runs on a two-year lookback. The income that determines your Medicare premiums at, say, 67 is generally your reported income from age 65. So a single big-income year can ambush you two years later, long after you have forgotten about it.

Why early retirees are not off the hook

It is tempting to file IRMAA under "future problem." We did, briefly. But the moves that trigger it are the exact moves early retirees make on purpose. Roth conversions. Realizing capital gains. Taking a lumpy distribution. Selling a property. All of those inflate the income the IRS sees in a given year, and if they happen at 63, 64, or 65, they can echo straight into your first Medicare premiums.

There is also the longer arc. If we do not convert or draw down our tax-deferred accounts at all, required minimum distributions eventually force income out whether we want it or not, and those forced withdrawals can park us in an IRMAA bracket for years. So the question is not whether to manage income, but when.

This is where the tax view in RetireOdds earns its place in our daily planning. We can see our projected income year by year and exactly where the IRMAA thresholds sit. When a planned conversion would tip us over a cliff, it shows up before we do it, not two years after, when the premium notice arrives.

How we think about the cliffs

Our working approach, and this is education rather than advice, is to treat the thresholds like guardrails on a mountain road.

- We map the IRMAA brackets for the years that will feed into our Medicare premiums.

- When we plan a Roth conversion or a gain harvest, we size it to stop short of the next cliff rather than blowing past it.

- We try to spread income-generating moves across multiple years instead of stacking them into one, so no single year gets ambushed.

None of this means avoiding income. Sometimes paying a surcharge is worth it, for instance if a large conversion now prevents much larger forced income later. The point is to make that a decision, not an accident. The friend who got burned did not weigh the surcharge against the benefit. He simply did not know the line was there.

Because we span currencies and countries, the moment we cross into Medicare years is also tangled up with our broader income picture, which is one more reason we wanted everything in a single view instead of scattered across calculators that each see only part of the story.

Key takeaways

- IRMAA is an income-based surcharge on Medicare premiums, and it works as a cliff: one dollar over a threshold bumps you to the next tier for the whole year.

- It uses a roughly two-year income lookback, so a big-income year can quietly raise your premiums later.

- The classic triggers, Roth conversions, capital gains, lumpy withdrawals, are exactly the tools early retirees rely on, so timing matters.

- Sometimes paying the surcharge is the right call; the goal is to decide on purpose, with the thresholds in view.

If Medicare is on your horizon, it is worth seeing where your projected income lands against those cliffs. Run your own odds and find the brackets before they find you.