The 8 Years Before Medicare Nobody Plans For

Retire before 65 and you bridge to Medicare on your own dime. Here's what that bridge really costs.

The first time we priced out early retirement, the spreadsheet looked great until Mona asked one question: "What do we do about health insurance until Medicare?" Mayur is 46. Medicare starts at 65. That is roughly 19 years for him, and even counting from a target retirement date, it is the better part of a decade with no employer plan and no Medicare card. For a US family of four, that gap is not a rounding error. It can be one of the three biggest line items in the whole plan.

What the bridge actually is

In the US, Medicare is the federal health program that kicks in at 65. Before that, if you have walked away from a job, you are on your own to buy coverage. That window between your last paycheck and your 65th birthday is what people call the bridge to Medicare. For someone retiring at 55, it is ten years. For us, depending on when we pull the trigger, it could be eight.

The reason nobody plans for it is that working people never see this cost. Your employer quietly pays most of your premium, so the number on your paystub is a fraction of the real price. The day you retire, that subsidy vanishes and the full sticker price lands on you.

Where the money goes

You have a few ways to cover the bridge, and they are wildly different in cost.

- COBRA lets you keep your old employer plan, usually for up to 18 months, but you pay the full premium plus a small admin fee. It is often the most expensive option, and it does not stretch eight years anyway.

- The ACA marketplace is where most early retirees land. You buy an individual plan, and crucially, the premium you actually pay depends on your income. More on that below.

- Going abroad is our wildcard. We have lived in Thailand, Singapore, and now Spain, and quality care in some of those places costs a fraction of US prices out of pocket.

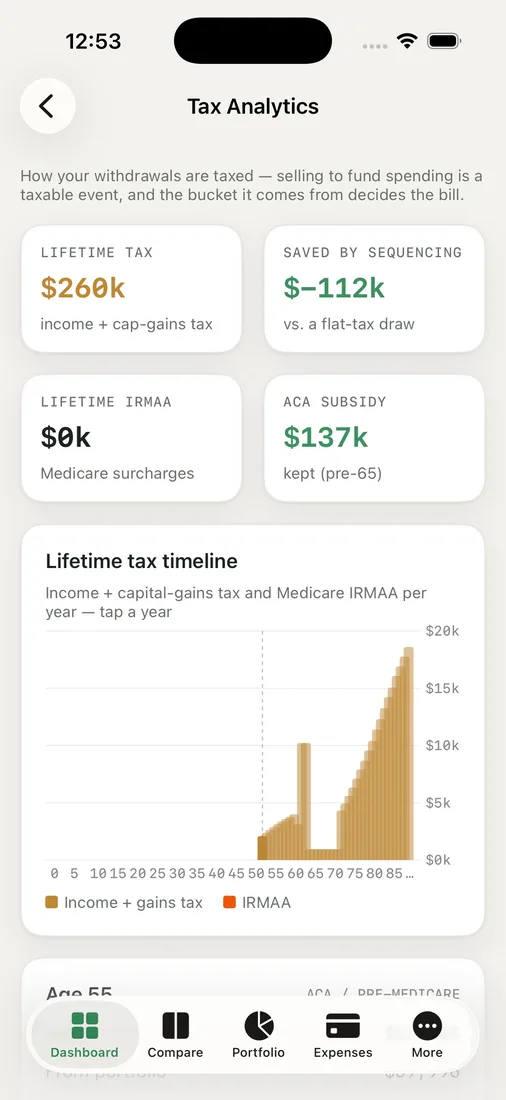

Here is the part that surprises people. On the ACA marketplace, your premium is tied to your modified adjusted gross income, not to how much money you have. A family showing $80,000 of income might pay a very different premium than the same family showing $55,000, even with identical savings in the bank. That means the way you pull money in early retirement, from taxable accounts, from Roth, from a little capital gains harvesting, directly moves your health insurance bill.

This is exactly why we built the tax and healthcare view in RetireOdds. We can see, year by year, how our planned withdrawals translate into reported income, and how that income lands us in or out of ACA subsidy territory before Medicare takes over at 65. It turned an abstract worry into a number we could actually steer.

The mistake we almost made

Our first plan front-loaded big withdrawals from our taxable accounts in the early years, the very years we would be buying insurance on the marketplace. On paper it was tidy. In practice it would have pushed our reported income up and quietly cost us thousands a year in lost subsidies. Same spending, same lifestyle, just a worse order of operations.

Once we saw the two pieces side by side, our withdrawal plan and our health premium, the fix was almost boring. We smoothed our reported income across the bridge years, leaned on Roth and cash for part of our spending, and kept ourselves in a friendlier subsidy band until Mayur ages into Medicare. Nothing exotic. Just sequencing we would never have spotted without watching both numbers at once.

We are not giving advice here, and your situation will differ, especially if part of your bridge happens outside the US like ours might. The point is simpler: the eight or so years before Medicare deserve their own line in the plan, not a hopeful footnote.

Key takeaways

- The years between early retirement and Medicare at 65 are a real, often large expense that working people never see, because employers hide most of the premium.

- On the ACA marketplace, your premium depends on your reported income, so how you pull money matters as much as how much you have.

- Front-loading taxable withdrawals in your bridge years can quietly cost you subsidies; smoothing reported income often helps.

- Living abroad for part of the bridge can change the math entirely, which is why a tool that handles geography and currency earns its keep.

If you are eyeing a date before 65, it is worth seeing your own bridge laid out year by year. Run your own odds and watch what your income choices do to the cost of getting to Medicare.