How Roth Conversions Lower Your Medicare Premium

Converting early can shrink later RMDs — and the income that drives IRMAA surcharges. Two birds.

When we first sketched our retirement decades out, we noticed something odd. In our seventies, our projected income shot up, even though we would not be earning a thing. The cause was a big pile of tax-deferred savings that the IRS will eventually force us to withdraw, like it or not. Those forced withdrawals threatened to push us into higher tax brackets and, worse, into Medicare premium surcharges. The fix turned out to live decades earlier, in the quiet years right after we stop working.

The setup: a tax bill waiting to happen

Money in traditional IRAs and 401(k)s has never been taxed. It grows untouched, which feels wonderful until you remember the government wants its cut someday. That someday arrives as required minimum distributions, or RMDs, which force a percentage of those accounts out as taxable income starting in your seventies.

For a diligent saver, RMDs can be a trap of your own making. The bigger the tax-deferred balance, the bigger the forced income, and that income does two unpleasant things at once. It can lift your tax bracket, and it can shove you over the IRMAA thresholds that raise your Medicare Part B and Part D premiums.

So the same diligence that built the nest egg can, left alone, raise your healthcare costs in your seventies and eighties.

The lever: convert in the low-income valley

Here is the maneuver, and we will keep it educational rather than prescriptive. A Roth conversion moves money from a traditional account into a Roth account. You pay tax on the amount you convert now, but it then grows tax-free, comes out tax-free, and never triggers an RMD.

The magic is timing. Early retirees often have a window of unusually low income. The paychecks have stopped, but Social Security and RMDs have not started. In that valley, your tax rate can be remarkably low. Converting during those years means:

- You move money out of the tax-deferred pile at a low rate today.

- You shrink the balance that will later be forced out as RMDs.

- Smaller future RMDs mean lower future income, which can keep you under the IRMAA cliffs and hold your Medicare premiums down.

That is the two-birds part. The same conversions that lower your lifetime tax bill can also lower the income that drives your Medicare surcharges years later.

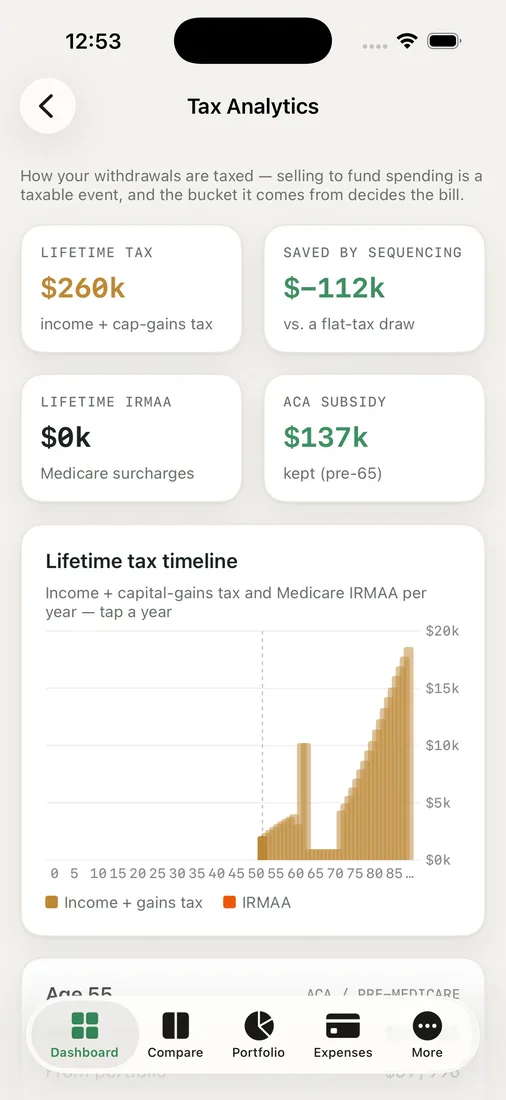

We do this planning right inside the tax view in RetireOdds. We can see the low-income valley clearly, watch how a conversion shrinks our projected RMDs, and check that we are not converting so much in one year that we trip an IRMAA threshold or, before 65, blow up our ACA subsidy. It is a balancing act, and seeing all the lines at once is the only way we have found to keep it honest.

The catch nobody mentions

Roth conversions are not free money. You pay the tax sooner, so converting too aggressively can hurt. There are real tensions to manage.

Before 65, big conversions can inflate the income that sets your ACA marketplace premium, undoing health savings on one side to chase them on the other. After 65, an oversized conversion can land you in an IRMAA bracket two years out. The sweet spot is usually a series of measured conversions that fill up a tax bracket without spilling over a cliff, repeated across several of those low-income years.

For our family, with money and reporting spread across countries, the conversion question is tangled up with currency and foreign-income rules too, which is part of why no off-the-shelf calculator ever fit. We needed to see the whole picture, year by year, and steer.

We are not telling you to convert. We are saying the years between your last paycheck and your first RMD are quietly some of the most valuable in your whole plan, and they are easy to waste by doing nothing.

Key takeaways

- Large tax-deferred balances eventually force taxable RMDs, which can raise both your tax bracket and your Medicare premiums via IRMAA.

- Roth conversions in the low-income years after retiring can shrink future RMDs, lowering both lifetime taxes and later Medicare surcharges.

- Converting too much backfires: it can wreck ACA subsidies before 65 or trigger IRMAA cliffs after 65.

- The usual approach is measured conversions that fill a bracket without crossing a threshold, repeated over several years.

If you have a tax-deferred pile and a quiet stretch ahead, it is worth seeing where your future RMDs land. Run your own odds and find your own low-income valley before it closes.