Fill the 12% Bracket on Purpose

Empty low-bracket space is a missed opportunity. We convert just enough each year to fill it.

Most of our working life, taxes were something that happened to us. We earned, the brackets did their thing, and we tried to deduct what we could. It wasn't until we modeled our early-retirement years that we saw something strange and a little thrilling: in some of those years, we'd have room left in the low brackets that we simply weren't using. Empty space we were allowed to fill at a bargain rate — and were about to waste.

That's the idea behind filling a bracket on purpose. It sounds backwards to volunteer for more taxable income. In the right years, it's one of the smartest things you can do.

Brackets are buckets, and they don't refill

Picture each tax bracket as a bucket. Income pours in from the bottom. The first bucket fills at a 0% effective rate thanks to the standard deduction. The next fills at 10%, then 12%, and so on. Your top dollar sits in whichever bucket isn't full yet.

The thing to understand is that the buckets reset every January and never carry over. If we only have, say, $30,000 of income in a year when the 12% bucket doesn't fill until much higher, all that low-rate space evaporates at year-end. We can never get it back.

In our gap years — retired, before Social Security, before required distributions — those low buckets will sit half-empty. So the question becomes: what cheap income could we deliberately create to fill them?

What goes in the empty space

There are two clean ways to use the room.

The first is a Roth conversion. We move money from our traditional IRA into a Roth, report it as income, and pay tax at that low bracket rate today. In exchange, that money grows tax-free forever and is never subject to required distributions. Every dollar converted in the 12% bucket is a dollar that won't get forced out later, possibly at a much higher rate.

The second is harvesting long-term capital gains. In the lowest brackets, the federal rate on long-term gains can be 0%. Selling appreciated shares and immediately rebuying them resets your cost basis upward without a tax bill — quietly erasing future gains.

Hitting the line without crossing it

The catch is precision. Fill the bucket and stop, and you win. Overfill by a few thousand dollars and that overflow gets taxed at the next rate up — and worse, it can nudge you over thresholds that have nothing to do with income tax: more of your Social Security becoming taxable, an ACA subsidy shrinking, an IRMAA surcharge switching on.

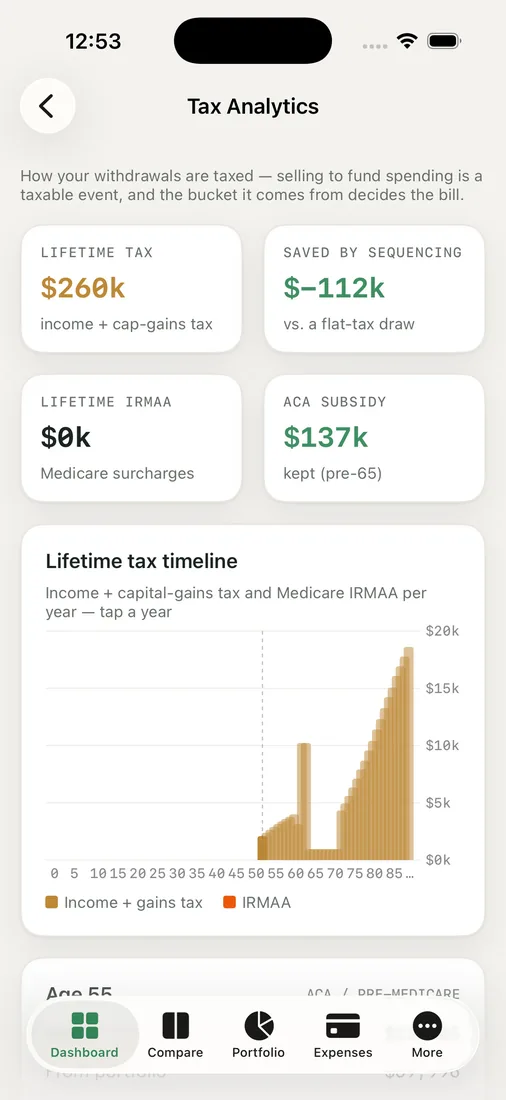

This is why we don't do it by hand. In RetireOdds, the Tax Analytics view shows exactly how much room is left in each bracket for each future year, after accounting for our other income. It tells us how big a conversion or gain harvest fits before we spill over.

Seeing it laid out year by year changed how we think. Some years have huge empty buckets; some have almost none, depending on what else is going on. The plan isn't a fixed annual number — it's a different deliberate top-up every year, sized to the space available.

A fair warning: the exact bracket figures, the gain-harvest math, and the interaction with subsidies and Social Security are genuinely fiddly and they change with the law. We use the model to ask sharper questions, then confirm the actual numbers with a tax professional before we pull any triggers. This is education, not advice.

Key takeaways

- Tax brackets are buckets that reset every year and never carry over — unused low-rate space is gone for good.

- In low-income years you can fill the bucket on purpose with Roth conversions or 0%-rate capital-gains harvesting.

- Overfilling spills into a higher rate and can trip Social Security, ACA, and IRMAA thresholds, so precision matters.

- The right amount to add is different every year, based on your other income.

Find out how much low-bracket room you're leaving on the table — run your own odds and see your empty buckets year by year.