Which Account Do You Spend First?

Taxable, tax-deferred, Roth — the order you withdraw in can save six figures over a retirement.

When you spend down a portfolio across countries and currencies, you spend a lot of time thinking about where money comes from. Early on, we assumed it didn't much matter which account we tapped first — money is money, right? Then we ran the numbers and discovered that the order of withdrawals, holding everything else identical, could swing our lifetime tax bill by a genuinely startling amount. Same spending, same lifestyle, same portfolio — wildly different tax outcomes, decided entirely by sequence.

Three buckets, three tax personalities

Retirement savings usually live in three kinds of accounts, and each behaves differently when you withdraw:

- Taxable brokerage accounts. You only owe tax on the gains, often at lower capital-gains rates, and your original contributions come out tax-free.

- Tax-deferred accounts (traditional 401(k), IRA). Every dollar out is taxed as ordinary income, and these are the ones that trigger Required Minimum Distributions at 73.

- Roth accounts. Funded with already-taxed money, so qualified withdrawals come out completely tax-free and never face RMDs.

Because each bucket is taxed so differently, the order you drain them in changes how much income shows up on your return each year — and your tax bill is driven by that yearly income, not your lifetime total.

Why the order is worth real money

The conventional sequence is taxable first, then tax-deferred, then Roth last. The logic is elegant: spend the lightly-taxed money first, let the tax-free Roth keep compounding longest, and leave the tax-deferred accounts in the middle.

But the conventional order isn't always optimal, and that's where the real savings hide. If you blindly drain taxable accounts first and let the tax-deferred balance grow untouched, you can walk straight into the RMD tax bomb in your 70s — a wall of forced ordinary income exactly when you have the least flexibility. Often the smarter play is to deliberately pull some tax-deferred money in your low-income early years, even before you strictly need to, to flatten that later spike.

Letting the engine sequence it

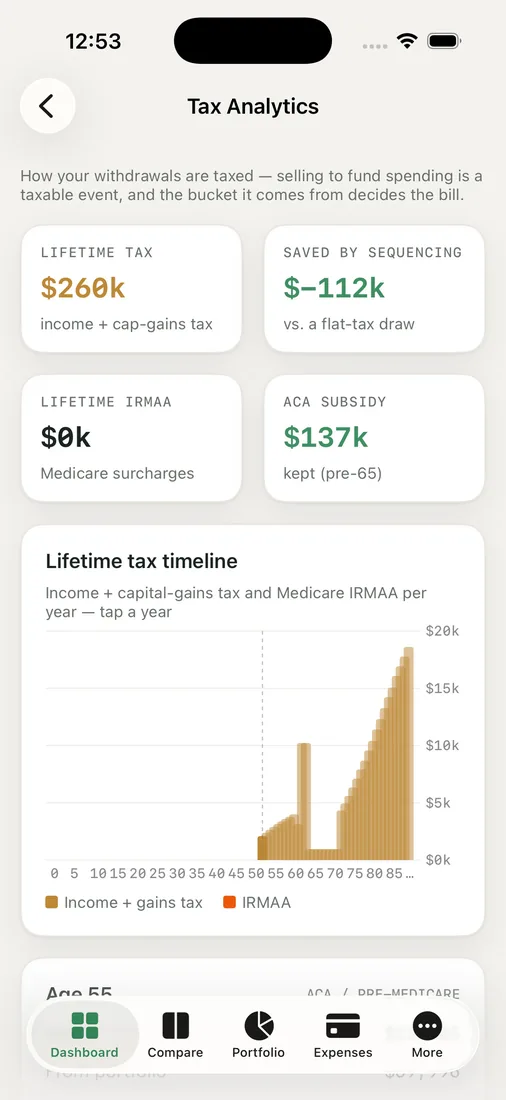

This is where the Tax Analytics view earns its keep. It's bucket-aware: it models pulling money in a sensible order across taxable, tax-deferred, and Roth, projects the lifetime income and capital-gains tax, and shows a figure we now obsess over — the amount saved by sequencing.

That single number reframed the whole exercise. We could see how a thoughtful order avoided bracket spikes, kept us under the IRMAA surcharge thresholds, and — because we manage health coverage through the ACA — stayed below the subsidy cliff that a careless big withdrawal could send us tumbling over. For an expat family, layering the Foreign Tax Credit on top, getting the order right isn't a nicety; it's one of the highest-return decisions we make.

None of this changes how much we spend or how we live. It only changes which account the money leaves from each year. That's what makes it feel almost like free money — the lifestyle is identical, and the only difference is how much of it the tax code takes.

Key takeaways

- Taxable, tax-deferred, and Roth accounts are each taxed differently, so the withdrawal order changes your tax bill without changing your lifestyle.

- The default "taxable, then tax-deferred, then Roth" is a starting point — sometimes tapping tax-deferred early flattens the later RMD spike.

- A bucket-aware projection shows the lifetime tax saved by sequencing, and helps you dodge IRMAA and ACA-cliff thresholds.

- Getting the order right can be one of the highest-return, lowest-effort moves in your whole plan.

See how much smart sequencing could save you — model the order and run your own odds.