How RMDs Can Push You Into a Higher Bracket

Required distributions can stack on top of Social Security and quietly raise your tax rate for decades.

The first time we projected our taxes out to age 75, we assumed the math would get easier with time. We'd be retired, the kids would be grown, the house would be paid off. Instead, the model showed our taxable income climbing in our seventies — higher than in some of our working years. The culprit wasn't a windfall or a mistake. It was the IRS forcing us to take money out of our traditional accounts whether we needed it or not.

That is the part of retirement nobody warns you about. The tax bill you spent decades deferring eventually comes due, and it tends to arrive all at once.

What an RMD actually is

When you save in a traditional 401(k) or IRA, you get a deduction today and a promise to pay tax later. "Later" has a deadline. Once you reach your required beginning age (currently 73 for most people, rising to 75 for younger savers), the IRS makes you withdraw a minimum percentage of those accounts every year. That percentage starts around 4% and climbs as you age.

Here is the trap. The required amount is based on your account balance, not your spending. If we have, say, $1.4 million in traditional accounts at 73, our first required distribution could be roughly $53,000 — money we have to report as income even if our actual expenses are lower. And because the accounts often keep growing, the dollar amount the IRS demands tends to rise year after year.

Why it stacks, and why stacking hurts

Income tax is layered. Your first dollars are taxed lightly; later dollars get taxed at higher rates. The question is never "what bracket am I in" but "what bracket does my next dollar land in."

An RMD lands on top of everything else. Picture the layers in order: Social Security for both of us, maybe a small pension, dividends and interest from the taxable account — and then the RMD piles on top. By the time it arrives, the lower brackets are already full. So the required distribution gets taxed at the highest rate we face, and it can shove ordinary income up into a new bracket entirely.

It gets worse. Higher income can make more of your Social Security taxable, can trigger IRMAA surcharges on Medicare premiums, and can raise the tax rate on your long-term capital gains. One forced withdrawal quietly raises the cost of several other things at once.

Seeing it before it happens

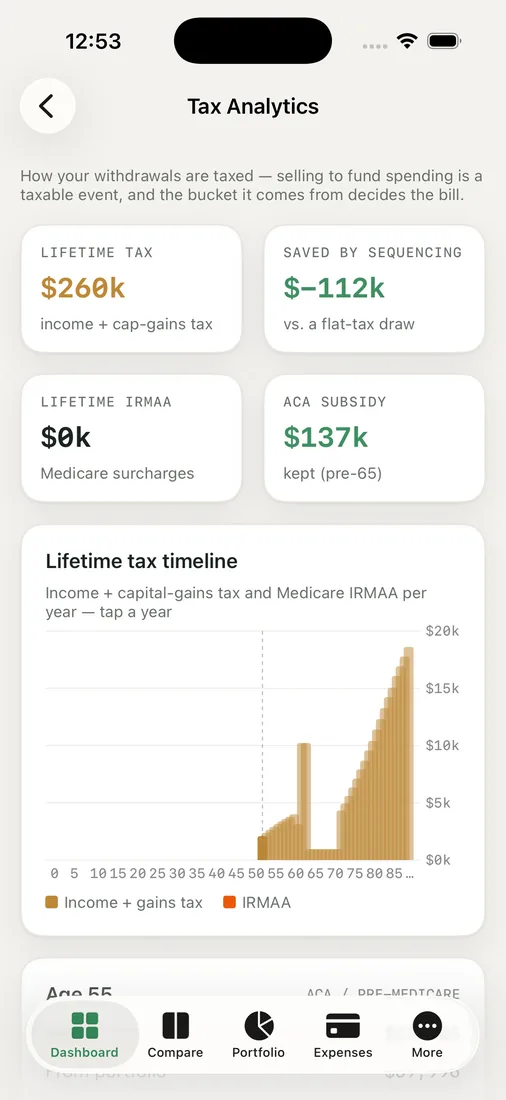

This is exactly the kind of slow-motion problem a spreadsheet hides and a projection reveals. In RetireOdds, the Tax Analytics view plots required distributions year by year, stacks them on top of Social Security and other income, and shows the bracket each future year lands in. Seeing those RMD bars grow into our seventies is what made the problem real for us.

The same view also shows the lever. The years before RMDs begin — for us, our late forties through early seventies — are often the lowest-income years we'll ever have. That window is where we can voluntarily move money out of traditional accounts at low rates, through Roth conversions, so the IRS has less to force out later. RetireOdds models that too, so we can watch a few thousand dollars of conversions today shrink the RMD bars decades out.

What we actually did with this

We didn't panic or drain the accounts. We treated it as a sequencing problem. Knowing the RMDs were coming, we started filling our low brackets on purpose in the quiet years, leaning on the taxable account for spending, and letting the projection tell us how much to convert before the forced withdrawals would have pushed us higher. None of this is advice — every family's brackets, balances, and state situation differ, and this is the moment to bring in a professional. But it's a far better conversation to have at 46 than to discover at 73.

Key takeaways

- RMDs are based on your account balance, not your spending, so they can force out more income than you actually need.

- Because they stack on top of Social Security and other income, required distributions are often taxed at your highest rate — and can trigger IRMAA and higher taxes on Social Security and capital gains.

- The pre-RMD years are usually your lowest-income years and your best window to move money out of traditional accounts at low rates.

- A year-by-year projection turns an invisible future problem into a decision you can act on today.

The only way to know whether RMDs will quietly raise your rate is to look ahead — run your own odds and see where your income lands at 75.