The Tax Bomb Hiding in Your 401(k)

At 73 the IRS forces withdrawals whether you need them or not. Here's how we're defusing ours early.

We spent a decade feeling smug about our 401(k) and traditional IRA balances. Every contribution was a tax deduction; every year the number grew tax-deferred. It felt like winning. Then we actually modeled what happens at 73, and the smugness evaporated. That growing pre-tax balance isn't entirely ours — a chunk of it belongs to the IRS, and at 73 they come to collect on a schedule we don't get to set. That's the tax bomb, and as US citizens living abroad, ours has a few extra wires.

What the tax bomb actually is

Money in a traditional 401(k) or IRA went in untaxed, so every dollar that comes out is taxed as ordinary income. As long as it stays put, the balance compounds — and the eventual tax bill compounds right along with it.

Then come Required Minimum Distributions. Starting at 73, the IRS forces you to withdraw a rising percentage of those accounts every year, whether you need the cash or not. The problems stack up fast:

- Those forced withdrawals can push you into a higher tax bracket in your 70s and 80s than you ever paid while working.

- The extra income can trigger IRMAA surcharges that raise your Medicare premiums.

- For us, there's a cross-border layer too — US taxes our worldwide income, and the Foreign Tax Credit only partly cushions the overlap.

The cruel irony is that the more successfully your pre-tax accounts grow, the bigger the bomb gets.

Seeing the bomb before it goes off

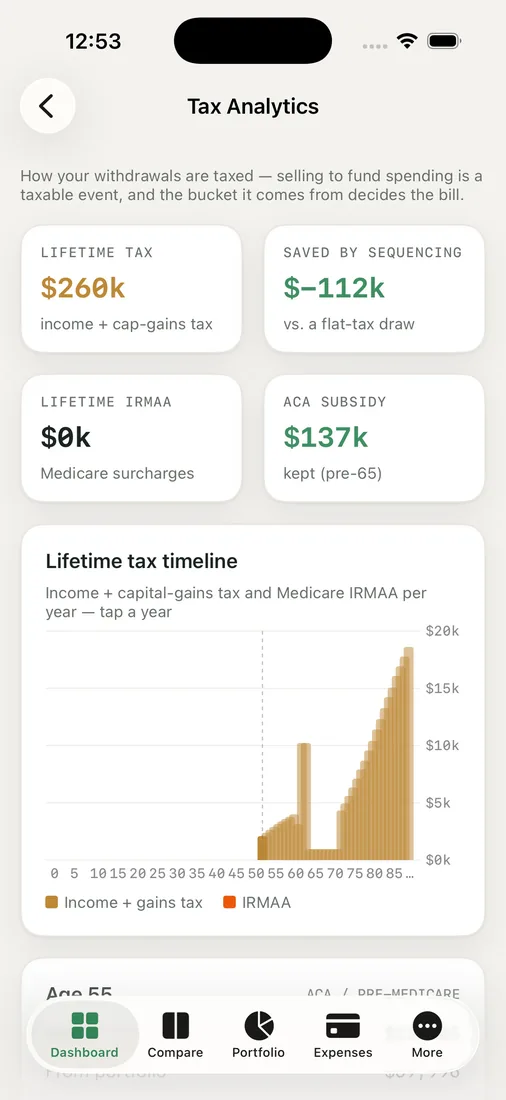

This is exactly what the Tax Analytics view is for. Instead of looking at one year, it projects our lifetime income and capital-gains tax, models the RMDs, and shows how the bill clusters in our 70s if we do nothing.

Seeing it laid out across a lifetime was the wake-up call. A wall of forced income in our 70s, IRMAA surcharges riding on top, and a tax rate higher than today's — all of it visible years before it would actually hit. The number that had felt like pure victory suddenly had a price tag attached.

Defusing it early

The good news is that a bomb you can see is a bomb you can defuse. The main tool we're using is Roth conversions during our low-income early-retirement years — the stretch between when we stop working and when RMDs and Social Security kick in. In those years our tax bracket is unusually low, so we can move money from the traditional accounts into a Roth, pay tax now at a low rate, and shrink the future forced withdrawals.

The Roth conversion ladder in RetireOdds plans this year by year, filling up the low brackets without spilling into the high ones or tripping the IRMAA and ACA thresholds we also have to watch.

We won't pretend conversions are free — you pay real tax in the year you convert. But moving money out at a low rate now, to avoid forced withdrawals at a high rate later, is the whole game. Defusing the bomb early, in the quiet years, beats letting it detonate on the IRS's schedule.

Key takeaways

- Traditional 401(k)/IRA balances carry a deferred tax bill that grows with the account.

- Required Minimum Distributions at 73 force taxable withdrawals that can spike your bracket and trigger IRMAA surcharges.

- Look at lifetime tax, not a single year, to see how the bill clusters later in life.

- Low-income early-retirement years are prime time for Roth conversions that fill low brackets and shrink future RMDs.

See the bomb hiding in your accounts — model your lifetime tax and run your own odds.