What 'Good Enough' Odds Actually Look Like

100% success is a trap. Here's the confidence level we actually plan around — and why.

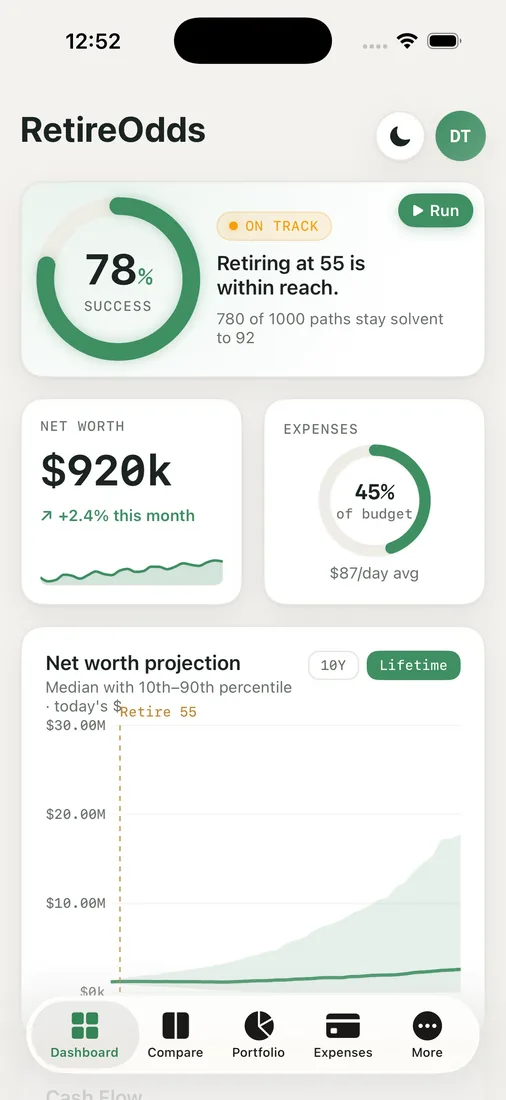

For a while, we were chasing 100%. Every time the dashboard showed our plan succeeding in, say, 92% of futures, Mayur would reach for the sliders to close the last gap. Spend less, work longer, anything to get the gauge to read perfect. It took us an embarrassingly long time to realize that the chase itself was the mistake. A demand for certainty was quietly making our actual lives smaller — and it was chasing a number that doesn't really exist.

Why 100% is a trap

A 100% success rate sounds like the goal. In practice it's a warning sign. To make a forty-year plan survive every simulated future, including the genuinely catastrophic ones, you have to spend so little or work so long that you've over-saved for a disaster that probably won't happen. You buy insurance against the 1-in-100 future by sacrificing the 99 ordinary ones.

There are two more honest problems with it:

- The model isn't reality. Even a 1,000-path simulation can't include every possible future. "100%" is 100% of the scenarios we modeled, not of the ones that can happen.

- Life is adjustable. A plan isn't a rocket launch you can't change after liftoff. If a bad stretch hits, real people trim spending, work a little, or adapt — which means you don't need to pre-fund the apocalypse.

The number we actually plan around

So we stopped aiming for perfect and started aiming for resilient. The dashboard gives us a clear read on where our plan stands, and rather than treating anything under 100% as failure, we look for a strong, comfortable margin with room to breathe.

A high-but-not-perfect success rate, to us, means the plan holds in the overwhelming majority of futures, and the handful where it doesn't are the kind we could respond to in real time. That's not settling. That's matching the precision of the answer to the precision of the question — because nobody can promise certainty about forty years of markets and life.

What a "good enough" margin buys you

The most freeing realization was that the distance between a very strong plan and a "perfect" one is rarely safety — it's mostly extra years of work or a meaningfully smaller life. Once we could see that trade-off on the dashboard, the choice got easier. We'd rather hold a robust margin and start living than grind toward a last few percentage points that mostly insure against scenarios we'd adapt to anyway.

We still watch the number. We still want it strong, and we'll trim or adjust if it drifts low. But we no longer treat anything short of 100% as a problem to eliminate. We treat it as honesty — and honesty, it turns out, is what lets us actually retire.

Key takeaways

- 100% success is a trap: it forces over-saving against rare disasters and ignores that real plans can adapt.

- No simulation captures every future, so "100%" really means "100% of what we modeled."

- Aim for a strong, resilient margin with room to adjust, not flawless certainty.

- The gap between "very strong" and "perfect" usually costs extra working years or a smaller life — make that trade on purpose.

Find the confidence level you can actually live with — run your own odds.