How Much Can You Spend Without Going Broke?

Forget the balance — the number that matters is the safe annual spend your plan can actually support.

We track our spending across three currencies, and there's always a moment near the end of the month when Mona looks at the totals and asks the question that really runs our household: not "how much do we have?" but "how much can we actually spend without wrecking the plan?" Those are different questions, and confusing them is how comfortable-looking families quietly run out of money. The balance is the part everyone watches. The safe spend is the part that decides the ending.

Why spending is the real number

A portfolio balance is a snapshot. Spending is the flow that drains it, and it's the one variable you mostly control. You can't dictate market returns or inflation, but you can decide what leaves the account each month. That makes your spending rate the single most powerful lever in the whole plan.

The trap is that a generous-looking balance can support wildly different spending levels depending on how long it has to last and how rough the markets get along the way. Two families with the same savings can have completely different odds purely because one spends more than the other. So "how much can I spend without going broke" isn't a lifestyle question — it's the central math of retirement.

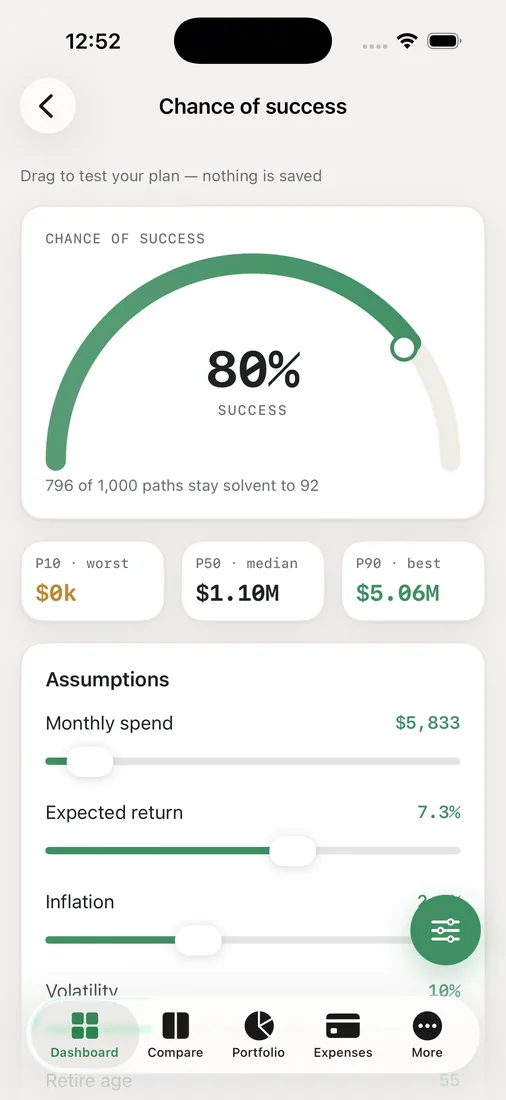

Finding the safe spend

On the Chance of Success screen, we treat spending as the dial we turn. We set a monthly number, and RetireOdds runs 1,000 different futures to report the share where the money lasts. Then we move the spend slider and watch the gauge respond in real time.

That live feedback is the whole experience. Push spending up, and you can watch the odds slide as the gauge dips. Ease it down, and the odds climb. Somewhere in that range is the level where the plan holds up even in the unpleasant futures — and that, for us, is the actual "safe spend." It's not a fixed law; it's the point where we're comfortable with how the worst-case paths look.

Reading it in today's dollars

One detail keeps us honest: results come back in today's dollars. A spending number two decades out can look huge in raw figures and buy surprisingly little. By inflation-adjusting everything, the gauge tells us what our money will actually do at the grocery store, not what it looks like on paper. For a family whose costs float with exchange rates, that grounding matters.

Spending that bends

The other thing we learned is that "safe spend" doesn't have to be a single rigid figure. A flexible approach — spending a bit more after good years and trimming after bad ones — usually supports a higher average spend than a rigid, fixed-dollar plan, because it stops forcing withdrawals into falling markets. Watching the odds under different spending styles changed how we think about our own budget.

We don't aim to spend the absolute maximum the gauge allows. We aim for a number that leaves the worst-case paths looking survivable, and then we live inside it without that end-of-month dread.

Key takeaways

- Spending, not balance, is the lever that most decides whether your money lasts — and it's the one you control.

- Find your safe spend by turning the spending dial and watching how the odds respond, then plan against the bad-case paths.

- Read everything in today's dollars so future figures don't flatter you.

- Flexible spending usually supports a higher sustainable average than a rigid fixed-dollar withdrawal.

Find the number you can actually spend — run your own odds and move the dial.