Inheritance: Lump Sum vs. Lifetime Income

An inheritance is a one-shot. How we model turning a lump sum into decades of reliable spending.

When Mona's family went through an estate a couple of years ago, the inheritance that came to us was a meaningful sum — and it arrived with a weight we didn't expect. This wasn't money we'd earned and could replace. It was a one-shot, carrying someone's whole life of saving. Spend it badly and there's no second paycheck to fix the mistake. The question we sat with wasn't "what can we buy?" It was "how do we make this last?"

An inheritance is the purest test of a hard idea: how do you turn a single lump sum into decades of reliable spending?

A lump sum is not income

The instinct is to treat a windfall like income — a big number you can draw against freely. But a lump sum and an income stream are different animals, and confusing them is how inheritances quietly disappear.

Income refills. A lump sum doesn't. Every dollar you pull from it is gone, plus the growth it would have earned over the rest of your life. The real question is what rate of spending a fixed pile can support before it runs dry across a long horizon — and the answer is far lower than most people guess, because it has to survive bad markets, inflation, and a retirement that might run 40 years.

There's also a behavioral trap. A lump sum feels like permission. It loosens the grip on spending precisely because it's so large — and "we can afford it, it's an inheritance" is the sentence that ends a lot of inheritances.

Turning the pile into a paycheck

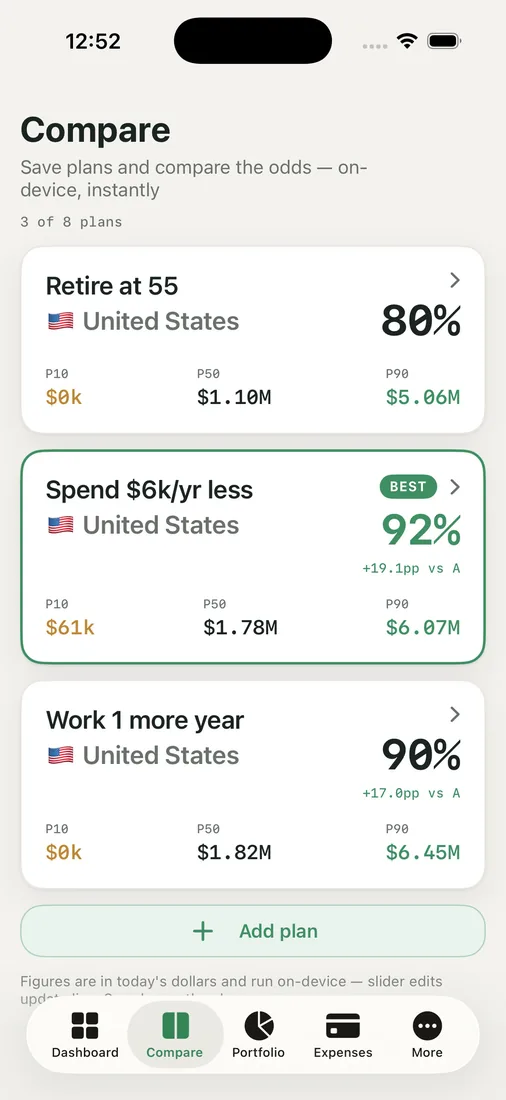

We modeled it instead of feeling it. In Compare Plans, we built two scenarios:

- Spend it down — fold the lump sum into the portfolio and let our existing spending rise to absorb it.

- Turn it into income — treat the inheritance as a dedicated engine for a modest, sustainable annual draw on top of our base plan.

Each came back with a success percentage and a "BEST" badge. The difference was stark. Letting spending drift upward to "use" the windfall chipped away at our long-run odds — the pile shrank faster than it could grow. Converting it into a disciplined lifetime draw barely moved the spending dial year to year, but it raised our odds and, more importantly, the money was still there decade after decade.

That reframing — from "a lot of money now" to "a little more money every year, forever" — is the whole trick.

The test that mattered most

A headline success number wasn't enough for money this irreplaceable. We took the "turn it into income" plan into Chance of Success and ran the 1,000-path Monte Carlo, watching the P10 path — the unlucky-market case — and the today's-dollars view so inflation didn't flatter the result.

The lifetime-income approach held up even on the gloomy path. That's the bar we wanted for a one-shot: not "works if markets cooperate," but "works even when they don't." A windfall you can only spend in good markets isn't security; it's a bet wearing security's clothes.

For us as expats there was one more wrinkle: the inheritance and our spending live in different currencies, so we kept the dual-currency view on to make sure the draw stayed sustainable in the money we actually spend, not just the money we received.

Key takeaways

- A lump sum is not income — it doesn't refill, so the real question is what sustainable annual draw it can support across a long horizon, which is lower than it feels.

- "Spend it down" usually erodes your odds as lifestyle creep absorbs the windfall; converting it into a disciplined lifetime draw preserves both the odds and the money.

- Test the income plan with a Monte Carlo and judge it on the unlucky-market path in today's dollars — irreplaceable money deserves the stricter bar.

- If the inheritance and your spending are in different currencies, check sustainability in the money you actually spend.

Sitting with a one-shot windfall? Run your own odds and see what lifetime paycheck it can really pay.