How to Pay $0 Federal Tax in Retirement (Legally)

With the right bucket order and the standard deduction, a surprising amount of retirement income is tax-free.

When we tell people we expect to pay little or no federal income tax in some of our early-retirement years, the reaction is usually a raised eyebrow — as if we're describing a loophole. We're not. It's the plain reading of the tax code, applied to a household that controls where its spending money comes from. A family spending $70,000 a year can, in the right years, owe close to nothing to the IRS. The trick isn't aggressive; it's the standard deduction plus a little discipline about which account you tap.

The first slice is already free

Start with the standard deduction. For a married couple it shields tens of thousands of dollars of income from tax entirely. That's not a deduction you have to chase or itemize — it's automatic. The first chunk of ordinary income each year effectively sits in a 0% bucket.

Then there's the special treatment of long-term capital gains and qualified dividends. In the lowest brackets, the federal rate on those is 0%. So a couple can realize a meaningful amount of long-term gains, on top of the standard deduction, and still owe nothing.

Stack those together and a surprising amount of cash flow comes through tax-free before you've done anything clever at all.

The clever part is the buckets

The reason most retirees don't get near $0 isn't the law — it's the account they draw from. Pull everything from a traditional 401(k) and every dollar is ordinary income; you blow past the standard deduction quickly and start owing. Pull from the wrong place at the wrong time and you create a tax bill you never needed.

We think of our money in three buckets:

- Taxable — a regular brokerage account, where only the gain is taxed, often at that 0% long-term rate in low-income years.

- Tax-deferred — traditional 401(k) and IRA, where every withdrawal is ordinary income.

- Roth — already taxed, so withdrawals are completely tax-free and don't even show up as income.

A near-zero-tax year is usually built by blending these. Draw enough traditional money to soak up the standard deduction (free), harvest long-term gains up to the 0% ceiling (free), and top up whatever spending is left from Roth (invisible to the IRS). Same $70,000 of spending — radically different tax bill depending on the mix.

Watching the year come together

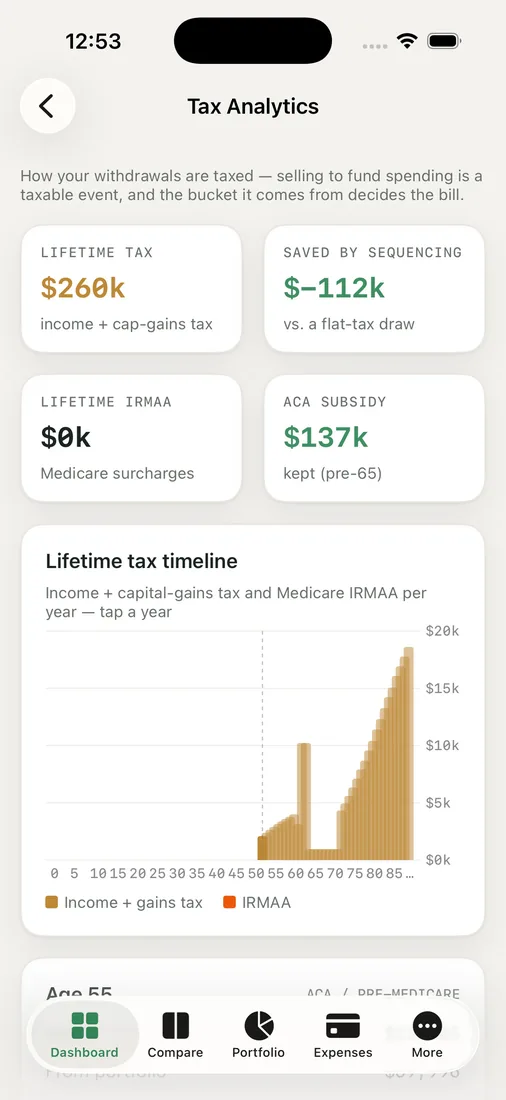

This is fiddly to do by hand because the buckets interact and the thresholds move. In RetireOdds, the Tax Analytics view models the bucket-aware withdrawal order for us — taxable, then tax-deferred, then Roth — and shows the resulting federal tax for each future year. When a year lands at or near zero, we can see exactly which slices made it happen and how close to the edge we are.

The honest caveats matter here. A "$0 tax" year is often not the goal. Sometimes it's smarter to deliberately pay a little 10% or 12% tax now — by converting to Roth or harvesting more gains — to avoid much higher rates once required distributions and Social Security arrive. A perfectly zero year can be a wasted-bracket year. The model helps us decide when zero is the win and when filling the low bracket beats it.

And to be clear: this is education, not advice. State taxes, the ACA subsidy math abroad and at home, and your specific account balances all change the picture, so we run the projection and then confirm the moves with a professional.

Key takeaways

- The standard deduction plus the 0% long-term capital-gains rate already shields a large amount of income from federal tax.

- Whether you actually pay near $0 depends on which bucket you draw from — taxable, tax-deferred, or Roth — not just how much you spend.

- Blending the buckets each year lets the same spending produce a very different tax bill.

- A $0 year isn't always optimal; sometimes paying a little now beats a lot later, so look at the whole lifetime, not one year.

See which of your years could come in near zero — run your own odds and watch your federal tax change with the bucket order.