Retire Now vs. Work Three More Years

Three extra years of work can swing your odds more than you'd think. We put both plans side by side.

There's a specific kind of argument that early-retirement couples have, and we've had it more than once over dinner in three different countries. One of us wants to pull the trigger now. The other wants "just three more years" of income for peace of mind. Both positions are reasonable, both are a little emotional, and for the longest time neither of us could prove anything. We were trading feelings about money, which never ends well.

What finally settled it wasn't a better argument. It was putting both plans next to each other and letting the numbers talk.

Why three years swings so much

Working three more years sounds like a modest tweak. It isn't, because it pulls three powerful levers at once:

- You keep saving instead of spending, so the balance grows.

- You shorten the spend-down by three years, so the money has fewer years to last.

- You let the portfolio compound longer before you ever take a withdrawal.

Each of those alone helps. Together they compound, which is why a "small" delay can move the odds far more than people expect. The flip side, of course, is three years of your one life spent earning instead of living — and at 46 and 43, with kids who won't be kids much longer, that cost is real too. The point isn't that more work is always right. It's that you should know exactly what those three years buy.

Putting both plans side by side

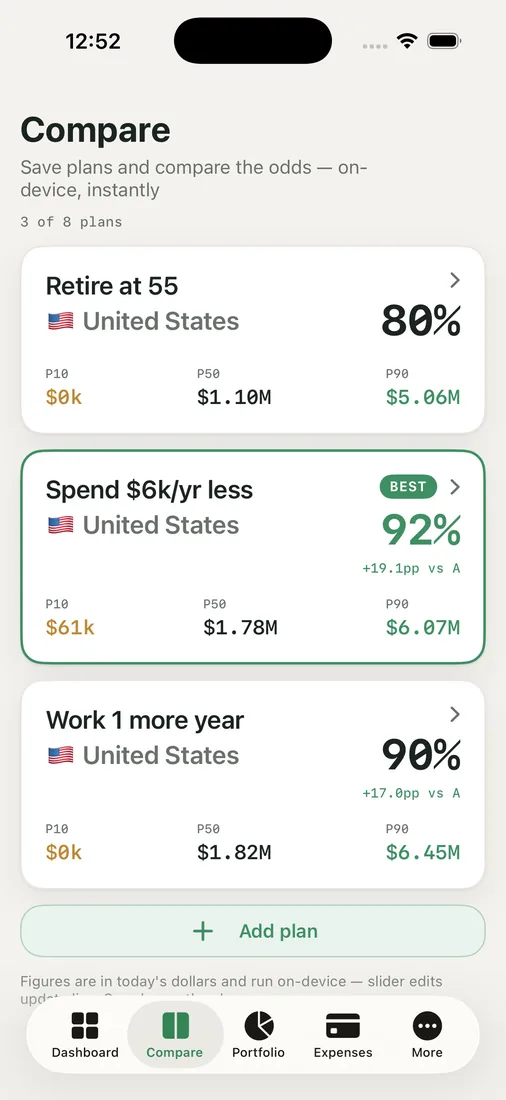

This is what the Compare Plans screen does for us. We save two scenarios — "Retire now" and "Three more years" — with everything else held identical, and each gets its own success percentage. The stronger one earns a BEST badge, so the comparison isn't a vibe, it's a labeled result.

Seeing them next to each other reframed the whole argument. It stopped being "I feel nervous" versus "I feel ready" and became a concrete trade: this many percentage points of safety, in exchange for those three years.

The settings that change the verdict

Compare lets each scenario carry its own assumptions, and a few mattered a lot for us. The Social Security claim age moves the later-life income floor. The country and expat settings matter because our costs and taxes don't live in one place. And the withdrawal strategy — constant dollar, fixed percentage, dynamic SWR, or Guyton-Klinger guardrails — can swing the odds as much as the retirement date itself. Sometimes "retire now with a flexible strategy" competed surprisingly well with "work three more years on a rigid one."

What we actually learned

The honest result for us wasn't a clean victory for either side. Three more years did lift the odds — but a chunk of that lift could also be captured by spending a little more flexibly, or claiming Social Security at a smarter age, without donating three years to the office.

That's the real gift of comparing: it separates the years you need to work from the years you're working out of fear. We'd rather buy our safety with a smart strategy than with our calendar, and now we can see the difference instead of guessing at it.

Key takeaways

- Three extra years of work pulls three levers at once — more saving, a shorter spend-down, longer compounding — so it can swing your odds more than it seems.

- Put both plans side by side with their own success percentages instead of arguing from feelings.

- Withdrawal strategy and Social Security timing can move the verdict as much as the retirement date does.

- Some of the safety from "more years" can be bought instead with smarter spending — so you only work the years you truly need.

Settle your own version of this debate — run both plans and compare your odds.