Sold the Business. Will It Last 40 Years?

After a lifetime building one asset, the question flips: can the proceeds outlast a long retirement?

A close friend spent eighteen years building a company and then sold it. The day the wire cleared, he expected relief. What he got was vertigo. For two decades his job had been to make one asset grow; now the asset was cash, the growing was over, and a brand-new question took its place — one he'd never had to ask before. Will this last the rest of my life? He's 52. If he and his wife live into their nineties, "the rest of my life" is 40 years.

We've spent five years asking our own version of that question, so we sat down with him to do what we do: stop guessing and run the odds.

The question flips

While you're building a business, the whole game is accumulation. Reinvest, grow, repeat. Risk is something you take on purpose because the upside is yours to capture.

The moment you sell, the game inverts. Now it's about decumulation — drawing down a finite pile without running out — and risk stops being your friend. The skills that built the asset don't transfer to making it last. Founders are often brilliant at offense and have never once had to play defense over a 40-year horizon.

Two things make this especially treacherous after a sale:

- Sequence-of-returns risk. A bad market in the first few years of drawdown does damage a good average return can't undo, because you're selling depressed assets to live on. Founders, used to riding out volatility while accumulating, often underestimate how differently it behaves when you're withdrawing.

- Spending uncertainty. After a lifetime of reinvesting, suddenly you're funding a life, healthcare, maybe helping kids — over four decades of inflation. The number isn't fixed and it isn't small.

The honest answer to "will it last?" isn't yes or no. It's a probability.

Turning a wire transfer into a probability

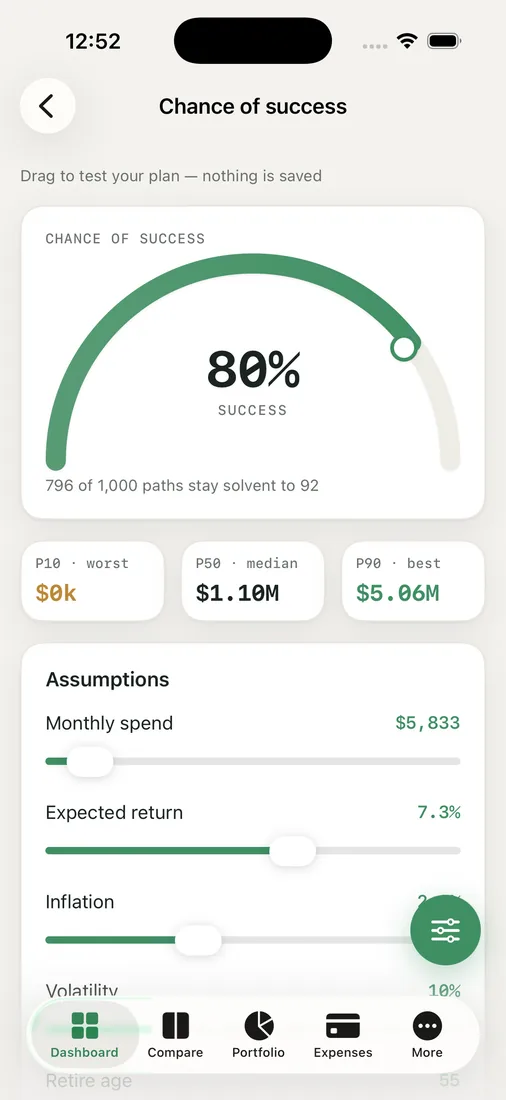

We put the after-tax proceeds and his real spending into Chance of Success and ran the 1,000-path Monte Carlo. That gives you a success percentage — the share of simulated 40-year futures where the money outlives him — and the P10 / P50 / P90 spread, all in today's dollars so inflation doesn't quietly flatter the result.

The median (P50) looked great, as it often does. But the number that mattered for a horizon this long was the P10 — the unlucky path where markets are unkind early. That's the path that tells you whether the plan is robust or merely lucky. For his draw, the P10 was tighter than he liked, which was exactly the useful, sobering signal he came for.

Because the horizon is so long, we also leaned on the historical sequence backtest engine — running his plan against real historical return sequences, including the genuinely brutal stretches. A plan that survives the worst sequences history actually delivered is a plan you can trust more than one that only survives a friendly average.

From "I hope so" to "here's the number"

The fix wasn't dramatic. We trimmed the initial spending slightly using the what-if sliders and watched the success percentage climb past his comfort threshold. A modest, flexible draw early — with the willingness to ease off in a bad first decade — moved the P10 from worrying to fine.

That's the shift every founder has to make after a sale. The wire transfer ends one game and starts another. The good news is the second game is winnable; it just rewards humility, a sustainable draw, and a clear-eyed look at the unlucky path instead of the rosy one.

Key takeaways

- Selling a business flips the game from accumulation to decumulation — different skills, and risk is no longer your friend.

- "Will it last 40 years?" is a probability, not a yes/no; run a Monte Carlo and judge the plan by the unlucky P10 path, not the comfortable median.

- For long horizons, stress-test against real historical return sequences — surviving the worst stretches history delivered beats surviving a friendly average.

- A modestly lower, flexible early draw can move the odds from worrying to robust; founders used to offense often underrate sequence-of-returns risk.

Just sold and wondering if it lasts? Run your own odds and turn the wire transfer into a real probability.