Spousal Benefits: The Strategy Couples Miss

For couples, claiming is a two-person optimization. The wrong order leaves real money on the table.

Mona and I are three years apart in age and, thanks to a career that wove in and out of full-time work while we moved countries, fairly far apart in Social Security earnings history. The first time we looked at claiming, we did what most couples do: we each pulled up our own estimate, picked an age that felt right, and added the two numbers. It was only later that we realized we had answered the wrong question. For a married couple, Social Security is not two separate decisions. It is one joint decision with two moving parts.

Why claiming is a couples problem

Social Security lets you claim as early as 62 or as late as 70. Claim early and your monthly check is permanently smaller. Wait and it grows, by a meaningful amount each year you delay past your full retirement age, up to 70. That part most people know.

What couples miss is everything that connects the two benefits.

There is a spousal benefit, which can let the lower earner receive up to half of the higher earner's full benefit if that is more than their own. And there is a survivor benefit, which means when one spouse dies, the survivor generally keeps the larger of the two checks, not both. Those two rules quietly rewire the whole optimization.

The survivor rule in particular changes the math. Whichever of us has the bigger benefit, that is the check the surviving spouse will likely live on for the rest of their life. Delaying the higher earner's claim does not just buy a bigger check for that person. It buys a bigger floor for the survivor, potentially for decades.

The order matters

Once you see it as a two-person puzzle, a common pattern emerges, and we share it as an illustration rather than a recommendation.

- The higher earner often benefits from delaying as long as possible, because that benefit becomes the survivor's lifelong income.

- The lower earner can sometimes claim earlier, bringing in some income now, especially if their own benefit is modest or a spousal benefit applies.

That is the "wrong order leaves money on the table" idea in a sentence. Two couples with identical numbers can end up with very different lifetime totals depending only on who claims when. Get the order backwards and you can shrink the survivor's floor by hundreds of dollars a month, forever.

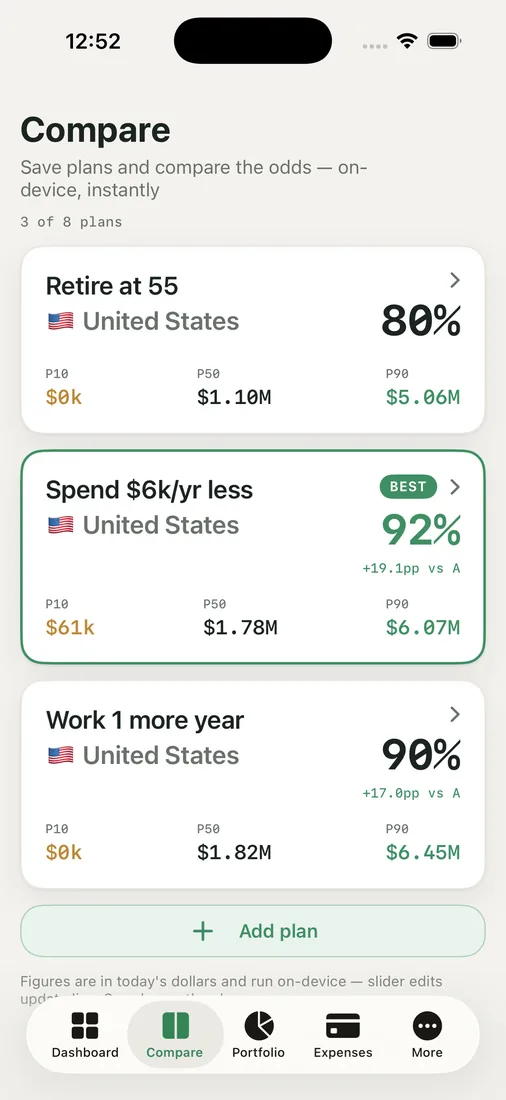

This is exactly what the compare view in RetireOdds is built for. We line up claiming scenarios side by side, say Mona at 64 and Mayur at 70 against both of us at 67, and each scenario reports its own success percentage for the whole plan, not just a benefit number. Instead of guessing, we can see how the order of our two claims ripples through decades of cash flow.

Don't forget the rest of the plan

The claiming decision does not live alone. When we delay the higher benefit, we have to fund those gap years from somewhere, usually our portfolio. That changes our withdrawal sequence, our taxable income, and even our healthcare picture before Medicare. So the "right" claiming order is not just whichever combination produces the biggest Social Security total. It is the one that fits the rest of the machine.

For us, the cross-border twist adds another layer. Years worked and taxed in different countries complicate the earnings record, and currencies complicate how we value a stable dollar benefit against assets held elsewhere. That is part of why we wanted to compare full scenarios, not just stare at two benefit estimates in isolation.

We are not advising any particular ages here, and every couple's earnings history, health, and longevity outlook differ. The takeaway is the framing: treat the two claims as one decision, weigh the survivor's floor heavily, and test the orders against your whole plan rather than your gut.

Key takeaways

- For married couples, Social Security is a joint decision, linked by spousal and survivor benefits, not two independent choices.

- The survivor generally keeps the larger benefit for life, so delaying the higher earner's claim raises the survivor's lifelong floor.

- The order of claims can swing lifetime totals substantially even when the underlying numbers are identical.

- The best order is the one that fits your withdrawals, taxes, and healthcare too, so compare full scenarios, not just benefit amounts.

If you are part of a couple, it is worth seeing your claiming orders tested head to head. Run your own odds and compare the scenarios before you lock one in.