The $6k/Year Cut That Adds 15% to Your Odds

In retirement, what you spend moves the needle more than what you earn. We measured exactly how much.

We spent years optimizing the wrong side of the ledger. Most of our planning energy went into returns — which funds, what allocation, whether to chase another half a percent. Then one evening we did something almost too simple to count as analysis: we shaved $500 a month off our planned retirement spending, $6,000 a year, and re-ran the odds. The success number jumped about 15 points. A whole afternoon of fretting over expense ratios had never done that.

Why spending is the stronger lever

There's a quiet asymmetry in retirement math. Your investment returns are mostly out of your control — the market does what it does. Your spending is almost entirely in your control. And in retirement, spending isn't a one-time decision; it's a number that repeats every single year and compounds against your portfolio for decades.

Cutting $6,000 a year does two things at once. It reduces the amount you withdraw, and it leaves more invested to keep growing. Over a thirty-year horizon those two effects stack. That's why a modest, permanent trim can move the needle more than a heroic year of stock-picking.

It's also why the trim has to be durable. A one-off cut barely registers. A $500-a-month change you can actually live with, year after year, is what bends the long-run odds.

What "15%" actually means here

We want to be careful, because numbers like "adds 15% to your odds" can sound like a guarantee, and nothing in retirement planning is guaranteed. Here's what we actually mean.

When we ran our plan, the Chance of Success gauge — the result of 1,000 simulated market paths — sat at one level. We then created a second version with spending lowered by $6,000 a year and changed nothing else. The gauge on that version landed roughly 15 points higher. For our inputs, on that day. Your number will differ. The point isn't the specific figure; it's the size of the effect relative to how little we changed.

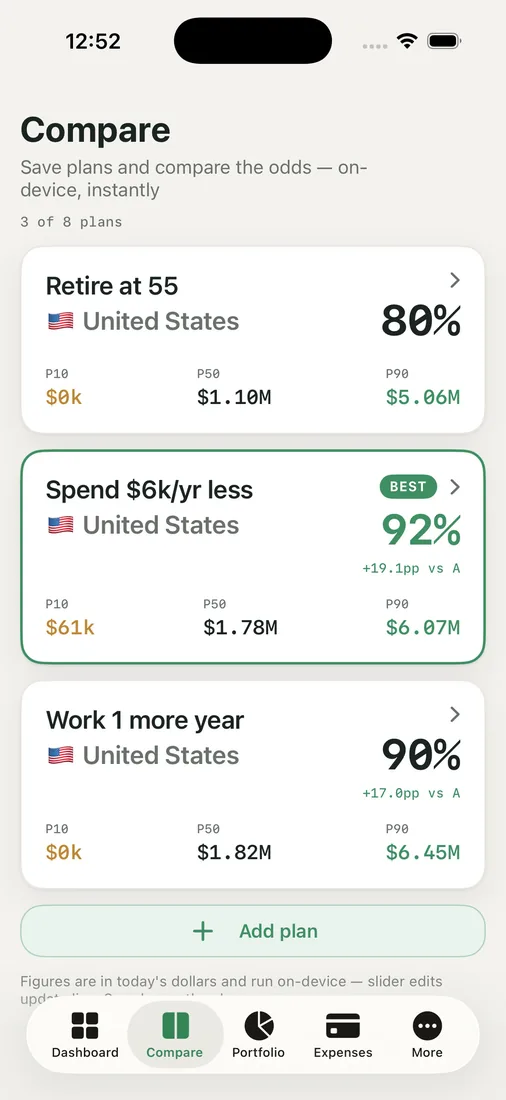

Seeing it in Compare Plans

The cleanest way to feel this is side by side. In Compare Plans we keep our base plan and a "spend a little less" plan next to each other, each carrying its own success percentage and a "BEST" badge on the winner. Two columns, one honest comparison. There's no story to tell ourselves — the gap is right there.

What we like about doing it this way is that it reframes the decision. It stops being "give something up" and becomes "buy 15 points of certainty for $500 a month." Suddenly the trade is concrete, and it's a lot easier to decide whether it's worth it.

The fast way to find your number

You don't have to build a whole second plan to get a feel for this. The single most useful control we have is the monthly-spend slider on the Chance of Success page. We drag it down a little and watch the gauge climb in real time; drag it back up and watch it fall. Within a minute you can find the spot where the odds reach a level you're comfortable with, and read off exactly what monthly spend gets you there.

For us, that slider turned an anxious, abstract worry into a dial we could actually turn. We weren't guessing whether we'd "saved enough." We could see the price of comfort, in dollars per month, and decide.

The whole exercise rebalanced where we spend our planning attention. We still care about our allocation. We just stopped pretending it was the biggest lever in the room. The biggest lever is the number we choose to spend, and it's the one entirely in our hands.

Key takeaways

- In retirement, spending is a more controllable lever than returns — and because it repeats every year, a modest permanent cut compounds against your portfolio for decades.

- A durable $500-a-month trim moved our success odds about 15 points in our example; a one-off cut would barely register.

- "Adds 15%" is illustrative, not a promise — re-run it with your own inputs to find your real number.

- The monthly-spend slider on the Chance of Success page lets you price comfort in dollars per month and dial in the spend that gets you there.

What does $500 a month do to your plan? Run your own odds and find your number on the slider.