Why Your 'Tax-Free' Withdrawal Isn't

To spend a dollar from a pre-tax account you often have to withdraw more than a dollar. Here's the gross-up.

For years we budgeted our future retirement the way most people do: add up the spending, multiply by 25, call it the number. We wanted to spend roughly $80,000 a year, so we figured we needed to pull $80,000 a year from our accounts. Then we ran the actual tax math and found a quiet leak. To put $80,000 in our pockets from our traditional 401(k), we'd have to withdraw quite a bit more. The difference goes to the IRS, and our original number was simply wrong.

That gap has a name. It's called the gross-up, and it's one of the most commonly missed pieces of retirement planning.

A dollar withdrawn is not a dollar spent

Money in a traditional 401(k) or IRA has never been taxed. The deduction you took on the way in was a loan from the government, and the bill comes due on the way out. Every dollar you withdraw counts as ordinary income.

So if you're in a bracket where withdrawals are taxed at, say, 12%, and you need $1,000 of actual spending money, you can't withdraw $1,000 — that only leaves you $880 after tax. You have to withdraw enough that what's left equals $1,000. The arithmetic works backward: divide what you want to spend by (1 minus your tax rate). At 12%, $1,000 of spending requires about $1,136 withdrawn. At 22%, it's about $1,282.

Why this quietly breaks plans

Stretch this over thirty years and the leak compounds. If your real after-tax need is $80,000 but you're actually drawing $92,000 or more to cover the tax, your portfolio is being depleted faster than your plan assumed. A success rate that looked comfortable can sag once the gross-up is included, because every withdrawal is bigger than it appeared on the spending line.

It's also why which account you draw from matters so much. A dollar from a Roth needs no gross-up — it's already been taxed, so a dollar out is a dollar to spend. A dollar from a taxable brokerage account is somewhere in between: only the gain is taxed, often at lower long-term rates. A dollar from a traditional account carries the full gross-up. Pull from the wrong bucket in the wrong year and you withdraw far more than you needed to.

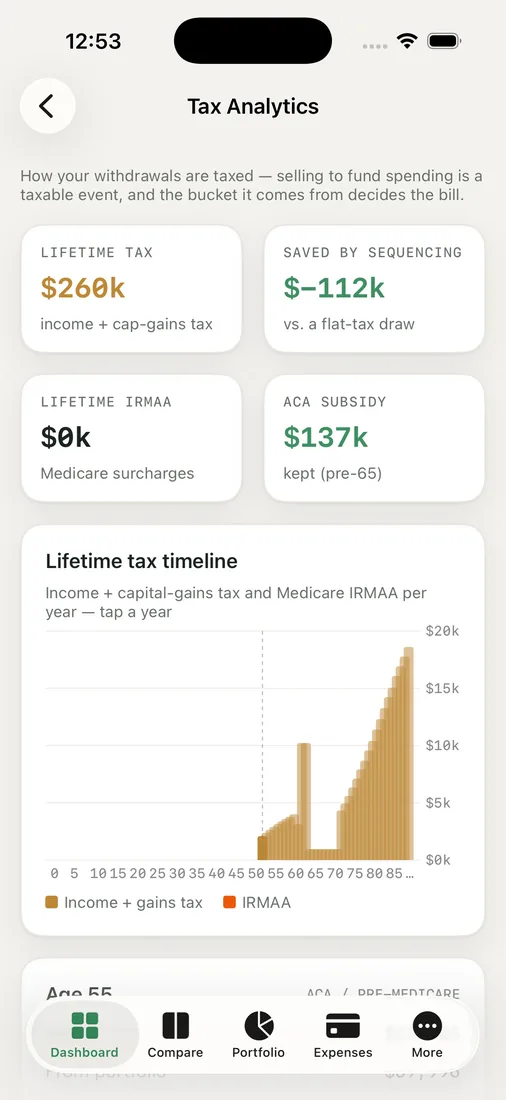

Where we see it

This is exactly the math RetireOdds does for us automatically. The Tax Analytics view doesn't just show our spending target — it grosses up each withdrawal, figures the tax bucket by bucket, and chooses a withdrawal order across taxable, tax-deferred, and Roth accounts to keep the lifetime gross-up as small as possible. There's even a "saved by sequencing" figure that shows how much we keep simply by drawing in a smarter order.

The first time we saw it, the lesson was humbling: our 25x number had silently understated what we needed, and the fix wasn't to save dramatically more — it was to sequence withdrawals so fewer of our dollars ran through the highest gross-up. A Roth in a high-income year, taxable gains in a low-income year, traditional withdrawals to fill the cheap brackets.

None of this is tax advice, and the right order depends on your brackets, your state, and your account mix — confirm the specifics with a professional. But the principle holds for everyone: budget after-tax, not before, or your plan is quietly too optimistic.

Key takeaways

- A withdrawal from a traditional account is taxed as income, so spending $1,000 requires withdrawing more than $1,000 — that's the gross-up.

- Plans that target spending without grossing up understate the real drawdown and overstate the odds of success.

- Roth dollars need no gross-up, taxable dollars are taxed only on gains, and traditional dollars carry the full hit — so withdrawal order matters.

- Sequencing withdrawals across buckets can meaningfully cut the lifetime tax you pay for the same spending.

See what your spending really costs once tax is included — run your own odds and check your number after the gross-up.